Why zoom out and lose the fidelity? So people who don't actually pay any attention to the axes/labels/etc. can walk away with a slightly better understand of the graph with their casual glance than they otherwise would have?

That's a stupid highbrow attitude. I suppose the same concept applies to any form of information? If we don't understand the whole story, it's not worth knowing any part of it?

It's disinformation. It's like when the meteorologist shows a map of temperatures across the region, not mentioning it is the 'feels like' temperature, an arguably useless and misleading number made up of the actual temperature and the wind speed. Just tell me the temperature and wind speed - let me be the judge of what it 'feels like'. Maybe I wear a windbreaker.

For sub-freezing temperatures with strong wind there is most definitely a point in mentioning wind chill factor. It keeps inexperienced people (i.e. tourists) from flooding the ER with frostbites. Otherwise I agree "the temperature it feels like" is silly.

I agree, if the interesting range of truck orders was 40000-50000 and the fluctuations between those values is the interesting information. However, here the article just mentioned the nose-dive to nearly zero at 2008, and then shows the graph where the number again dives to the x-axis. Then you take a second look and note it's a minor dip compared to 2008. The "interesting" range of truck sales had already been established in the article as 0-50000.

Arguing that axes should never be cut is silly indeed, but axes should also show the relevant ranges for the context (here the 2008 values for both x and y would make today's fluctuations look minor).

It's perhaps more egregious because the article leads with Volvo truck orders falling to approximately zero in a 99% one year drop.

This anchors the reader to misread 50% reductions from peak over the past five years and leaved reasons for the spikes which created the peaks unexamined.

One thing is clear is that the article doesn't point to a Volvo.

> In the third quarter of 2015, net sales for the Volvo Group amounted to SEK 73,309 M (67,222) with growth coming from North America and Europe. However, this was partly offset by a significant decline in South America. Adjusted for changes in currency exchange rates net sales

increased by 1% compared to last year.

The world economy is dominated by people in governments who believe that printing money, burying it and paying people to dig it up again will increase the amount of trucks built and goods shipped. No amount of failure of this theory will be enough for it to be abandoned, because it has a certain amount of truthiness to it, and it excuses profligate and wasteful behaviour. Both these things are fun and buy votes.

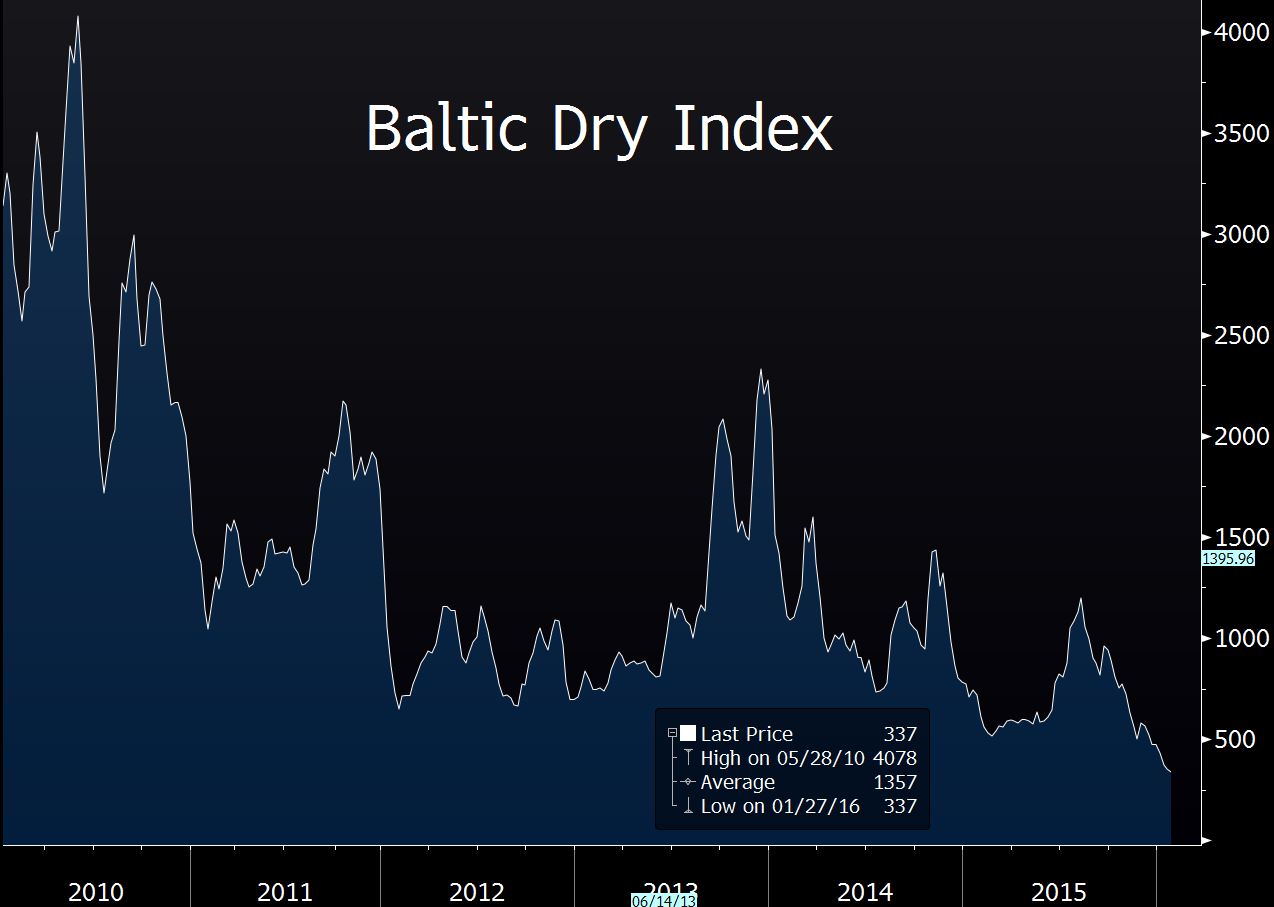

The Baltic dry should be studied in conjunction with other indicators such as yield curves and indications of credit tightness.

I absolutely will not defend Keynes or any other idea in economics, inasmuch as they can possibly be implemented in the political process that decide on economic policies.

That said, I do not think this is a case of a bad economist.

Economics theory is theory... theory that attempts to quantify societal behaviour, various cooperation dynamics, measurable output, etc. None of them know how to deal with various problems like "quality" & "technology" even though all economists admit they are pretty important. These theories usually have money playing a central role in some way). Anyway, they're theories about people acting together in big groups economics calls markets.

Political dynamics is another piece of the puzzle. So is every other meme in society. In some place homosexuals are allowed by society. In some places it is banned. Why now? Why not in 1750 or 2235? There are theories about how to quantify and predict here too, but obviously the ability of theories about such things are not up to the task of making consistent predictions.

Asimov's "psychohistory" is a fictional discipline which is basically economics, historical determinism, political science etc. The fictional twist is that these theories can make consistent predictions within very usable margins of error.

Monetarism is just a theory of the transmission mechanism going from money supply->price level->output, with some variations. Their policy proposals have been quite diverse.

Keynes himself had differing policy recommendations, as well, but ultimately settled on what he called "socialization of investment" where the state would fill in certain entrepreneurial activities that the private sector is deemed to be lacking, though the specifics were elusive. Contracyclical fiscal policy was actually popularized by Alvin Hansen IIRC, and the more extreme functional finance favored by Post-Keynesians was formulated by Abba P. Lerner.

There's is some government spending that has to be done anyway, but can be shifted in time so it's done when there's a recession.

Things like bridge rebuilding or warships.

Of course, if you're in recession for 8 years, you start running out of such things.

Funny thing is, there's plenty of rebuilding we could be doing, which would be quite stimulative, but it's politically unpopular because it would involve some tax and spend upfront, which would put a bit of a pinch on people in the middle and upper classes. Ironically, those same people stand to benefit from the lower classes having more discretionary income.

Many do. Not the sectarian economists hired to develop capitalist theology, but the ones you take seriously when you need to run a real capitalist economy. Here's a lucid explanation:

"If you take an economics course, they’ll teach you, correctly, that if the government spends n dollars to stimulate the economy, it doesn’t really matter what it’s spent on: they can build jet planes, they can bury it in the sand and get people to dig for it, they can build roads and houses, they can do all sorts of things—in terms of stimulating the economy, the economic effects are not all that different.² In fact, it’s perfectly likely that military spending is actually a less efficient stimulus than social spending, for all kinds of reasons. But the problem is, spending for civilian purposes has negative side effects. For one thing, it interferes with managerial prerogatives. The money that’s funneled through the Pentagon system is just a straight gift to the corporate manager, it’s like saying, “I’ll buy anything you produce, and I’ll pay for the research and development, and if you can make any profits, fine.” From the point of view of the corporate manager, that’s optimal. But if the government started producing anything that business might be able to sell directly to the commercial market, then it would be interfering with corporate profit-making. Production of waste—of expensive, useless machinery—is not an interference: nobody else is going to produce B-2 bombers, right? So that’s one point."

Funnily enough Chomsky is implicitly assuming that government spending has a crowding out effect, which is an idea popular with economists who are "hired to develop capitalist theology," as you label them.

But, probably not. Even "social spending" opens up lots of procurement opportunities for the corporate manager. There might be some crowding out in real terms (government having political authority to exclude activity it deems to be an interference), but it'll be offset by the likely benefits of ensuing expansion, corporate welfare grants and workforce mobilization.

The problem with Chomsky here and many others is that they have the causality backwards. They see corporations as evil entities that spontaneously emerged from the ground to usurp the state, when in fact they were explicitly cultivated by states looking for economic growth.

> "They see corporations as evil entities that spontaneously emerged from the ground to usurp the state"

This is the problem in an HN culture where commenters don't support claims with cites. Chomsky frequently explains that corporations are creations of the state, and they share the same interests to a first approximation. You can find it in the book I referenced, or google for sources.

This comment seems to paint him as a liberal who favors the state (blaming everything on corporations), when of course he's an anarchist who sees both state & its corporate creations as illegitimate top-down power structures.

In an interview, he clearly states that he favors maximization of state power in some narrowly defined "short term," and largely believes that the only alternative to a state is anarcho-syndicalism. He's relying on it withering away. [1]

I know full well he isn't a liberal and never implied that he's one (in the modern Galbraith sense). Nonetheless, most analyses by the revolutionary left are definitely slanted towards a picture of painting the issue as being primarily one of corporate hegemony.

they’ll teach you, correctly, that if the government

spends n dollars to stimulate the economy, it doesn’t

really matter what it’s spent on

Forgive my ignorance on these matters - I know that if the government pays a work crew the work crew ends up with money in their pockets regardless of what specifically they build; but surely if you pay a work crew to build a useful freeway or a bridge (or a rail system if you prefer) you also get the economic benefits of that freeway, bridge or railway; whereas if you pay the same work crew to dig a useless hole you don't get those economic benefits?

It's a popular idea but not borne out by the truth. In any decent sized (ie, not tax haven) economy, even the most financially distorted economy still produces a lot more real good and services than finance services.

The issue is that, by having politicians decide where and when to build the bridge, you don't necessarily end up with the right bridges.

What you wrote is correct, the flaw is you put in the word 'useful'.

If it were just about bridges and railways, it wouldn't be so bad. But lately economic stimulus is used as the fig leaf for all types of whole scale wealth destruction like cash for clunkers, amongst countless other examples.

But building / updating bridges, roads, rail networks, dams, lead water pipes etc. would have the side effect of being useful to the economy once built / updated.

Where I live billions and billions was spent on water infrastructure. No actual improvements in supply were made- no additional catchments were built, because dams == bad. The money was spent in pipelines and a desalination plant that has never - and I mean never - been switched on. It's 5 years old and has never output water, because the cost is too high compared to dam water.

Now I have a 400% increase in water bills but no actual improvement in what I get. That money goes to paying the interest and running costs for that investment. That money goes out of my local economy. That, in aggregate, prevents and extra shop from opening, or causes an existing one to close. Most businesses run in thin margins and diverting cash away on pointless make work lingers long after the supposed boost happens.

The effect of burying cash in the sand and hiring teachers are pretty much the same? I get what he's saying but it's glib to the point of being meaningless. Government spending doesn't buy just anything. Outlays are specifies by Congress to be done in the most efficient manner they can agree to (I know they suck at it, but that doesn't mean the theory is wrong). Nor is interfering with profitable business a concern when production and employment are shrinking as they do during a recession.

"If we discovered that, you know, space aliens were planning to attack and we needed a massive buildup to counter the space alien threat and really inflation and budget deficits took secondary place to that, this slump would be over in 18 months," he said. "And then if we discovered, oops, we made a mistake, there aren't any aliens, we'd be better--"

Except that you are left with a fleet of militarized space craft that provide no economic value and a pile of debt that was used to finance the fleet.

At that point somebody has to pay for that malinvestment through reduced future consumption. Make work projects are not a free lunch. They work by pulling demand from the future into the present via issuance of new debt.

How those costs are allocated in the future are delicate social issues with entrenched interests. In many cases these make work projects are themselves politically palatable ways to socialize losses by transferring bad debt from private balance sheets (households and corporations) to public balance sheets (government).

It could be argued that all economic cycles can be explained through malinvestment and then working through allocating losses.

My concern is that with activist central banks and fiscal policies that prefer to kick the day of reckoning into the future we have created a situation where allocating losses may lead to significant social and military confrontation (i.e. Revolutions and war).

Each round of centrally planned malinvestmemt in make work lowers the flexibility to deal with the next one, at the same time increasing the moral hazard for firms to expect the government to make good their losses. It also tends to create people dependent on governments as a source of livelihood, which robs them of economic agency.

All because a guy who actually didn't study economics waved away the long term structural issues by stating 'in the long run, we are all dead'

Besides, it's not economists that matter here. It's talking heads who provide cover for politicians to create massive amounts of malinvestmemt of scarce resources, diverting from possible productive investments and leaving behind the interest payments as a drag on future investment.

Boom & bust cycles are driven by the fundamental difficulty of quantifying value. Since there is no true value, people base their opinions on those of others (+delay), leading to "inertia," leading to oscillation. The government might exacerbate the oscillations, but the lion's share of responsibility lies with the market. Complaining that the oscillations happen because the market "just isn't free enough" represents a delusion about the qualities of free markets.

As for make-work, it's a compromise that nobody is happy with, but it is a compromise, and that's its value proposition. Some want to let the market clear without intervention by any means necessary, regardless of the social cost, based on (arguably misplaced) faith that this will ultimately make things better. Others think it's ridiculous that periodically attacking the foundation-tier Maslow needs of large swaths of the population is "a feature not a bug," and demand (arguably unsustainable) social policy to fix it. Make-work lies between the "free-market reckoning" and "re-distributional cash grant" extremes and so once the dust of democratic process has settled it's the thing that actually happens even though both sides see it as a poor alternative to their favored solution.

> The Baltic dry should be studied in conjunction with other indicators such as yield curves and indications of credit tightness.

The Baltic dry should be studied in conjunction with the reliable unreliability of the market in general. Since markets are as inherently unavoidable as physics or politics, we cannot simply wish them away. Instead, we should develop social policy to decouple the markets for well-understood core needs-providing infrastructure from the global economy in order to place bounds on the social cost of market corrections, which could then be allowed to happen (otherwise) unimpeded.

What you're describing might explain fluctuations, but it's inadequate and incomplete for the business cycle.

Virtually no one, not even Keynesian or other left-economists support make-work. It's mostly an idea favorable to laymen, or often done for more nationalistic rather than economic reasons. FDR was inspired by William Trufant Foster's and Waddill Catchings' policy advice for instance, who had Keynesian-esque underconsumptionist views but did not derive these from any economic theory per se.

Even ardent Keynesians will advocate a more sophisticated proposal of what amounts to government-owned employment agencies that combine private contract procurement with state investment projects, with the intention of having the unemployed serve as buffer stocks of labor to meet some form of output target. But not quite brute make-work.

(Actually the "quantifying value" problem makes no sense. It's not as if there is some objective essence called "value" that people seek. Value is largely denominated in units of currency. I suppose what you're getting at is the importance of monetary policy?)

But use value cannot be quantified, since utility is not a mathematical scale, but a subjective feeling that varies from person to person and with time as preferences shift or swing. I'm also unaware of how you can explain diverse business cycles throughout history as emanating from it.

Practically every economic theory that has tried to objectively quantify "value", i.e. those of Ricardo, Marx and Sraffa, relies on gigantic and complicated expositions involving leaps of abstraction and mathematical transformation problems that are completely detached from how real-world people actually think about or treat value.

(Indeed, such exercises in value theory aren't so much about determining value as much as trying to work out given theories of income distribution and perceived exploitation.)

I don't think our inability to quantify it means it's not objective. It means our mathematics is not advanced enough yet to capture use-value. Use-value is definitely objective as it is determined by nature. A screwdriver is useful because it screws screws.

Use-value is definitely context dependent and agent dependent. This is fine. But we have to acknowledge that the reason why people assign exchange-value to goods is because they have actual use-value: economics describes physical, real world activities.

I can agree that no one has presented a good dynamical theory of use-value. That's sensible: it would require at least a full description of reality, and a deep understanding of nonlinear mathematics. One quibble i have is i don't think Marx tried to establish such a theory: his observations about use-value and exchange-value can be made without a full theory of use-value or a full theory of exchange-value. The relationship between the two can be examined in the abstract and that is Marx's program.

I can still perform calculations with use-value to derive exchange value: why is water worth so little in exchange-value even though it is so vital to life? The marginalist point of view says that the price of water is determined by equilibrium between marginal cost and utility. Why is the marginal utility of water so low?

Well, if we're talking about people drinking water, then it is obvious, isn't it? You only have to drink so much water. When you're not thirsty, water has none of that use-value anymore.

Ignoring the relationship between use-value and exchange-value is... weird. It's replacing the true and difficult reality with a nice fiction amenable to manipulation with our primitive mathematics. Do markets define exchange-value or do they compute exchange-value from the aggregate use-values of everyone participating?

Edit: as for business cycles, i think they are caused by structural flaws in property rights and financial institutions, but if you asked 5 people why the business cycle occurs, you'll get 6 conjectures and 3.5 theories.

The marginalist conception of value is indeed underwhelming, but it's also a compromise. Determining value through mathematical exercises using hypothetical n-commodity worlds with homogeneous factors and units is at best useful as an exposition for a theory of income distribution (as Sraffa tried to do) in that by assuming a labor or commodity theory of value you can attempt to argue for a rate of exploitation.

Marxian economics has a whole lot of categories that are awkward, like "constant capital" being homogeneous and "variable capital" referencing wages of labor in producing commodities. There's barely any room for disequilibrium effects, complementarity, reserves and so forth. In turn, the organic composition of capital is held to be c/s+v, but empirical evidence on relation between OCC and crisis is scant and the concept of OCC is again completely foreign to uncertainty, disequilibrium and capital structure. It's just a ratio between two questionable taxonomies. Marxian economics has many similar failings as neoclassical economics, but because of its origins as a heterodox critique of Smith, Ricardo and Mill from a particular period, its evolution has been even more confusing.

Marginalism is situated in a means-ends framework, which is the most one can really say about value without introspecting into personal intentions and valuations. It should be underlined that neoclassical production theory (MC=MR) is separate from the subjective theory of value proper, however. Menger, Jevons and Walras all had different takes on it.

It's also worth noting that Marxian conceptions of use and exchange value have little to say about contemporary monetary and financial economies. Marxians still focus too much on issues like falling rate of profit, accumulation and OCC and often miss elephants in the room like financial fragility, or downplay them. It strikes me as archaic.

Whether or not markets compute or define exchange value seems to me like a problem of overaggregation where the contemporary social institution of a "market economy" is conflated with a market in the abstract as a system of mutual exchange, as in Proudhon and others.

My understanding is that FDR's "make-work" policies weren't only that - they were involved in massive infrastructure improvements which paid economic dividends, and building out parks, which provide cheap entertainment for the public. Perhaps there were others that were less useful, though?

FDRs policies included the Hoover dam, a massive productivity boost.

The latest round of stimulus spending included cash for clunkers, lots of money for financial institutions and paybacks to teachers unions and other supporters. That's not a partisan criticism, an administration of the opposite party would have given to their supporters in equal measure.

The rules of startups are about : make something that people want, and don't take money for the sake of it, your better of solving problems out of necessity.

The truth is that, as a theory, the idea works. In practice, it doesn't because it relies on the idea that central planning can work at all, and that lots of productive projects are available but can't get started due to lack of capital and resources. If a dam or bridge makes sense, then build it the moment it makes sense.

>Boom & bust cycles are driven by the fundamental difficulty of quantifying value. Since there is no true value

I disagree with this statement. Although I do agree that it is hard to quantify or even estimate value, all things do have a true intrinsic value relative to the utility they can provide human beings.

Entire empires have been built based on the concept of intrinsic value. Berkshire Hathaway is probably the most famous.

Boom and bust markets are caused by human infallibility and time lags.

Instead of providing government cover for the cycle, the lesson for businesses should be that they need to prepare for boo and bust. Knowing a truckload of government money will splash down the chute only increases moral hazard for reckless investment.

Your last paragraph sounds like a central planning nightmare. We don't need people in government buildings drawing lines around core needs. People faced with scarce resource allocation will make the choices that are right for themselves. Anything else ends up with tractor and leather shoe 5 year plans which don't match what people want.

Central banks are the problem. They have destabalised the global economy by constantly lowering interest rates and creating asset bubbles to promote the illusion of growth.

Central bankers are politically appointed in many cases so they have no interest in cooling an economy. It messes up the business cycle and creates the conditions for even bigger booms and busts.

Alternative currencies like Bitcoin will rise in popularity and may hold the key to a less manipulated financial system in the longer term - but I fear we will have another financial crisis before the new alternative currencies have gained traction. We shall see...

Central banks and automatic stabilizers are what have avoided a bigger crisis this time.

That doesn't mean that monetary policy is the right solution. The right solution is fiscal policy (government spending) but this is not happening because politics is dominated by crazy ideas about austerity and fiscal balances.

I'm not so sure. Central banks helped cause the 08 crisis by lowering interest rates after 9/11 and encouraging a housing bubble.

Their response to the 08 crisis (bailing out the banks, ultra-low interest rates, QE) may have laid the ground for an even bigger crisis further down the road.

All this is good news for alternative currencies IMO.

Indeed. You can measure boat and rail traffic, but what about the digital economy?

http://www.aei.org/publication/its-official-a-lost-decade-fo... :

"One potential explanation that reconciles these observations is that structural changes in the US economy may have resulted in a statistical understatement of real GDP growth. There are several possible areas of concern, but the rapid growth of software and digital content—where quality-adjusted prices and real output are much harder to measure than in most other sectors—seems particularly important."

At least now, yes. It was certainly an odd market before, somewhat segregated from other industries, but now technology is the driver behind all sorts of market moves - from lower prices to lower costs and higher profit margins to being part of almost every advantage one competitor gains over another.

I think people imagine "technology" is only Uber et al and can still be segregated into its own market, but some of the most interesting tech developments and software engineering are happening far from the Silicon Valley app-culture.

Hmm. I would buy that it wasn't easy to include it into economic models but it wasn't impossible and for a long time it's been an important factor to understand economy. Right now it's practically impossible to say anything relevant about the economy without because we don't have a model that includes technology.

Usually plummeting commodity prices are not a sign of economic activity, although they are priced in dollars so maybe a stronger dollar has something to do with it... but a strong dollar itself might suggest a flight to safety instead of global economic activity:

Perhaps worse for people in the US than a potential drop in exports (we've had a negative balance of trade for a while, irrespective of dollar strength) is the effect on corporate earnings for US companies that make money abroad. A strong dollar wreaks havoc on their balance sheets (since they need to report their earnings in dollars) and can absolutely lead to falling share prices as well as domestic job cuts.

China had an outsized affect on comkodity demand, at the same time capacity has been over built for many years. For oil, obviously the US resurgence has been a huge factor, and for food crops they had a couple of very very good years globally (and new land has been brought online).

Several currencies are sliding down against the USD (for a variety of reasons).

Food crops may be good but food prices are the first thing to spike when inflation spikes, and many nations have seen food prices climb ~20% across the board without parallel increases in wages and salaries. This is not good.

The BDI is a summation of a lot of information into a single price point. Megaships, and the general push for more fuel efficiency in new ship builds do impact it to some extent, but not to the degree necessary to account for a major push down.

Megaships, in general, don't work for the general shipping case. They work well for oil and containers where clients are either purchasing a small segment of the ship and their goods fit in 40' containers or they're buying millions of barrels of oil and need to move it halfway around the world. These ships are also port/canal limited. Most of the megaships cannot traverse the Suez or Panama canals and get forced to take the long way around, which can increase shipping time, and many of them cannot use most ports in the world. The new megacontainer ships are extremely limited because existing ports need to spend a significant chunk of capital to increase their capacity. Oil tankers, on the other hand, can lighter off the coast and either use offshore booms to transfer to shore via undersea pipelines or offload onto smaller tankers who take it into port.

The biggest driver in shipping costs is fuel. Yes, shipping is efficient in a tonnes/gallon ratio sense, but it still ain't cheap to fill up the tank. As oil prices plummet, it reduces the costs of operating tankers which increases the profit margin for the operating company and allows them to reduce prices in order to gain business. The second biggest driver is business. Companies position their assets where business is and if a lot of people have put their ships near the business, the business can negotiate a lower rate which will push the BDI down in price.

Source: I've built systems designed to track the maritime shipping market and the impact on commodities.

I invested a little in Dry Bulk right after the recession. The reason it's out for the count is a lot of players entered the market on expensive debt at the height of the Recession, taking the long bet that shipping would recover, which it did.

There was a brief glimmer of hope a few years ago when most of these companies refinanced their debt. The P/E ratios for most of these companies are incredibly low, but even still they are a bad investment. The structure of a lot of these companies is odd as well. They are often structured as shell companies wrapped around a private entity that actually employs everyone and does all the work. I'm guessing some companies have some pretty nice, debt financed, salaries for upper management.

Given the glut of shipping supply, and our current, modest recovery, I find BDI's tulmult to be less surprising than the sun rise this morning.

A rule of thumb is trucking spends 1/3 on fuel, more efficient rail spends 1/4 on fuel. Shipping is even more efficient, so its likely under 1/4 total costs.

(edited to emphasize that if fuel cost magically dropped to zero, costs could not drop more than perhaps 20%. And fuel has dropped, but not to magical zero)

All great points. Thing is you just provided additional support to the idea that premise in the article is flawed :)

Volume would be a much more important indicator.

qaq's assertion that shipping costs have zero correlation with oil prices is not accurate. It's not difficult to demonstrate that some correlation exists, and one can also do an overlay of shipping cost indexes to oil prices.

Shipping is already highly efficient in general, so it might be the opposite that fuel prices are a significant percentage of operating expenses. Low estimates I've seen state that fuel costs are around 40% of operating expenses. Source: https://people.hofstra.edu/geotrans/eng/ch7en/conc7en/bdi.ht...

I'm not arguing they're the only cost, but there has been a lot of hysteria about the Baltic Dry Index this month. So much that Snopes and Marine Traffic responded to it: http://www.snopes.com/cargo-ships-atlantic-map/

This reminds me of Ted Cruz's statistical "evidence" that over a 17 year period, the Earth is not warming. Because he started his 17 year period by including an unusually warm year, thereby significantly changing the outcome of the average. Had he looked at a 16-year or 18-year average, his "evidence" works against him.

Also like the "lesswrong" folks who use statistics to make grand claims. Statistics is not a looking glass. It is a math that is only as useful as the wisdom of its practitioner, and can lead to false confidence.

Because I don't need that many physical goods as I used to? My phone shows me temperature, map, music player. I can buy tickets which I don't need to print. I read book on Kindle. I don't need a car - I have a bike, public transport and Uber. As a result I need to rent smaller apartment.

Also factor in the trend of millennials living at home and declining family formation.

But the main reason for the drop is the collapse of the emerging markets and the fact that China has dramatically slowed down.

Rail traffic plummeted in December also, extremely low even though there is clearly a seasonal dip during that month. 2016 is starting off lower than the previous 3 years as well.

Last time this happened it was due to letters of credit abruptly being unavailable because of a worldwide bank crisis, due to a derivatives crash. Without letters of credit, nothing gets shipped. That's not what's happening today.

Low demand for commodities, also reflected in low prices, is driving the price of bulk shipping down. There's lots of slack capacity. But no problem getting a letter of credit if you are moving things.

The sky is not falling. This is Bear hype. A group he's connected with is probably short the market. Wait for the Black Swan to trigger just like the Bear Stearns trigger of last downturn. Keep an eye on the yield curve, the most important indicator. It's not bending yet.

I see these bears come out of the woods everytime they beat the "the bull run has been too long" drums.

As I understand the term "black swan", it isn't something for which one can wait. If a particular event occasionally happens at a particular point in a business cycle, then we can assign a rough likelihood to that event, and it isn't a black swan.

Sensationalist headline, nowhere is mentioned the oil glut. No point of moving oil if countries don't need it(why no need is another story, shale & warm weather).

I'm no stats major, but it seems like saying that an ~8k drop in orders from Q42014 to Q42015 is equal in some way to a ~41.7k drop in orders in 2008 is slight exaggeration.

There are a number of people who are perplexed. And that leads to a lot of speculation. There is also seems to be a strong survivor bias in economic reporting so everyone wants to be on record as both foretelling doom and not-doom, then depending on what happens they hope you'll remember they were "right".

Either way, there are interesting questions here which are unanswered. Like why do companies have so much money in their cash accounts? Generally, if a company is accumulating cash it isn't re-investing to grow. And while that might mean a planned acquisition of some other company the phenomena has gone on long enough that this seems less likely [1]. So why the cash hoard? For people it might be a 'rainy day' fund but does anyone believe that these companies will sit there, paying salaries, while selling few goods, waiting for the demand to return?

Or is it that the rent seeking transactions have become such a burden that it has been completely damping out new demand? One of the interesting thoughts is that if you go back and fix copyright and patents such that their terms expire in a more reasonable amount of time, or in the case of patents they are carefully scruitinized, then you take away this rent stream from big content and a number of license funded entities, that forces them to go out and make new content, or come up with new patented things, rather than just collect license fees. That creates new economic activity and that boosts GDP. It is a point of view that is gaining some adherents as a drag on economic growth.

Shipping as a leading indicator though has a couple of problems, both with isolating improvements in the industry (supermax ships) and shifts in modalities (air freight being acceptable for high margin goods like iphones) and generally the way consumption and manufacturing is changing (China's economic growth has zero impact on shipping if they pulling their bulk goods in over land and shipping locally).

Mostly though I suspect that there are lots of things that are unprecedented and so folks who are trying to plan are in a world of hurt in terms of confidence in their predictions. And like the reference to the movie in the article, it is always safer to predict doom and then report on "avoiding" it, than to mis-predict non-doom and to have it land at your feet. Hence more and more economists are saying "The world economy is toast!" rather than "I wonder if this is what it looks like at the leading edge of the switch away from a scarcity economy?" Sure, we could be approaching the singularity/jackpot what have you, but if you say that and the instead you get the biggest economic depression ever, well that is a worse outcome for the predictors.

[1] In an related note, having 10s of billions of dollars in cash means a company can do dozens of "10 - 50M" acquihire type deals, and that is driving some of the seed investing thinking I believe.

A lot of those oversized cash accounts can be explained by corporate tax structures that hold cash overseas in subsidiaries. Repatriation of that cash would incur significant penalties.

Pundits also suggest that shareholders who should be the beneficiaries of the cash through dividends are content to let CEO's and boards invest the cash for them due to a lack of other compelling investment opportunities.

Cynics might say with the prevalence of index and other funds who hold shares by proxy and who tend to vote with corporate management there is little pressure for CEOs or Boards to return funds to shareholders and instead hold them as a personal insurance policy and to extend their power base.

That is certainly a big part of it. But fundamentally it is idle capital. Why doesn't Apple build a German development center? I'm sure they could fill it with solid engineers and they could make it close to the auto centers and put their self driving electric car project there. Or pretty much anywhere in the EU. No need to repatriate funds if you can invest them in the area where they are already sitting and repatriate them as engineering expertise work items.

I'd be surprised if there was a large contingent of unemployed machine learning specialist sitting idle in Germany waiting for Apples investment dollars to unleash them. A billion dollars or even ten billion won't materilize the required skills in the requisite time.

An economist suggests this is an example of a skills mismatch.

The best indicator for anything transportation is utilization and how much stuff is actually being moved. Not just the price of moving something from A --> B. Yes, the presence of more movers, as the article points out, suppresses the price because people are competing to offer the lowest possible price to get the business. And, shippers did start investing in new builds extensively when it looked like the economy was set to go boom again which is also having a negative effect price due to the presence of more hulls on the market.

Unfortunately, the amount of stuff being moved is not public record and stays locked away on internal books that get summarized for the quarterly financials if the company is publicly traded. Which means we can infer how much stuff is being moved by reported dollar value but that's a lagging indicator. This leaves us with price to move goods as the major inference point to determine the health of commodities shipping and if the price is crashing, it's usually an indicator there's not a major uptick in the demand for commodities. When the price skyrockets it indicates people are trying to move a ton of stuff quickly and there isn't capacity to do it (causing more hulls to be built) and indicating the economy is hopping.

I came here to ask about whether or not we could see more than just Volvo's numbers? Apple releases numbers quarterly no? How are those doing?

And then Volvo is obviously not raw goods, but this article talks a lot about raw goods which I would presume to slowing with China's economic slow down (for how long can one build ghost cities).

My layman's analysis is that the US is in a pretty decent spot right now with a decently diversified economy but lots of other nations around the world are going to have to pull some smart moves if they'd like to sustain decent growth, but economics is a vast vast field with a seemingly unending number of indicators, so I may be totally off.

Excuse me if my questions aren't sophisticated to someone with a better understanding, I do literally plead ignorance here.

Volvo's order book (future orders) is indicative of how shippers see demand for new capacity. If I see demand increasing, I increase my purchase of capital assets (trucks in Volvo's case) to capture the business. If I see demand decreasing or holding constant, I withhold my large capital expenditures and ride my existing fleet as long as possible. It's already a sunk cost and all I'm paying for, at that point, is maintenance/overhead which get included in the rate for the truck.

At a macro level, when we see demand for future transportation assets decreasing that gives us insight into the transportation market and how people who provide the services see it going. They won't buy massive quantities of new goods if they don't see any business. Yes, companies like Apple release quarterly numbers, and we have to examine them in the context of their industry. Apple focuses on consumer electronic goods. As their numbers adjust and change, that gives us insight into (past) demand for consumer electronic goods and the state of the general consumer's purchasing power. You get leading insight into what Apple thinks demand will be, to some extent, by looking at their suppliers. Watch Samsung/TSCM when they announce big contracts from Apple. That gives you an inference as to what Apple thinks demand will be for a product. Same thing with shipping and transportation. Look at the industries that supply the goods and services transportation companies have to make capital expenditures to acquire and you'll get a rough idea of what the companies are thinking the market looks like.

Economy wise, yes, it's complicated to get a finger on the pulse of an economy and a lot of what goes into it. Technology and information travels over cables and electromagnetic waves and we've increased the efficiency of the manufacturing process to such an extent that we can use less people to sustain a higher rate of output than previous generations. However, there are fundamental factors that go into any economy you can measure to get an idea of what's happening and that usually takes the form of commodities. We need raw resources like food, energy, precious metals, and manufactured consumer goods to sustain the economy and most of those goods require special transport equipment to get from the suppliers and manufacturers to the consumers. Monitor that and you get a pulse on the overall health of the economy. The more facets you can monitor (trucks, rail, ships) the better your understanding.

You can also infer how much is being moved (on a very broad scale) in the US by the on-time record of Amtrak. They do not own the rails, and yield to any freight trains. When less freight is being moved, their on-time records improve.

Yes, you can get very general macro insights from metrics like that--if they're publicly available--but they are kind of worthless from a understanding point of view because they don't tell you what/where/when/who. The federal government does something similar with imports/exports for energy. But it's voluntary surveys and not guaranteed to be reliable. Especially since how much someone moves is competitive info.

It's more interesting to know that JP Hunt increased their lettuce hauling business from California to Missouri than it is to know that trucking tonnage creeped up ir down. That doesn't give you insight into the why or what's happening behind the scenes.

Is global trade reverting to the mean? Yes. Does that make it "toast"? No. The media treats every market correction as a crash much to the delight of value investors and bottom feeders. Hysteria is a great time to buy.

Seriously, I'm grabbing as much VFINX as I can. It's priced at February 2014 levels right now. That's a silly price for two pretty good years of global economic growth.

According to that chart, the beginning of 2012 would have been a horrible time to an invest and the market was about to enter a massive correction. Except the S&P is actually up >50% from 2012.

Here are more useful numbers: containers moved in and out of the Port of Los Angeles.[1] That's where most stuff from China enters the US. Monthly and annual numbers are available. Here's this decade:

2010 7.8 million TEUs

2011 7.9 million TEUs

2012 8.1 million TEUs

2013 7.9 million TEUs

2014 8.3 million TEUs

2015 8.1 million TEUs

So 2015 was down 2.5% from the peak.

The discouraging number in this is that half the containers going out of LA are empty. Only 3% coming in are empty. That's the US export/import imbalance. And a lot of the ones leaving the US are full of paper and metal scrap.

(One TEU is a "Twenty foot equivalent unit", or a 20' long container. A forty foot container, the most common size now, is 2 TEU.)

{kind=link}

{kind=link}

reply