I’m remortgaging next year and with interest rates as they are and what they’re predicted to be, I’ll be paying off only interest. I’ll be back to paying rent essentially. It’s a scary thought.

I don’t know how people (not 4%) are surviving.

How would the housing market bubble bursting affect people in this same situation?

Please don't accuse me of being a boomer, but I view interest rates as finally getting back to normal.

When I bought my first house in the early 2000s, mortgage rates were in the 6-7% range. I remember my parents had a 13% mortgage in the 80s. Its only in the last few decade or so that we've seen these 5% or lower rates. I think we just have to get used to it, and maybe the AirBnB crash will help at least lower the price of the house and make things more affordable..

The difference is that wages have not kept up with inflation nor with productivity and house prices are much higher. And another big problem is that the whole thing was poorly managed. People built lives around low interest rates, and people that were responsible got screwed over. I don't see how we suddenly flip that. Expectations were not clearly communicated.

I often feel like a lot of social policy is simple as long as people understand the tradeoffs and everyone is on the same page. Unfortunately that has not been the case.

I'm hoping the recent trend towards more active, powerful unions that we're starting to see now will reverse the wage trends.

The problem is that the very low interest rates we've had over the last decade are just not sustainable long term. At the very least, the Fed needs a quick, easy way to stimulate the economy, and having a minuscule prime rate leaves them without the biggest tool in their toolbox.

Unions will only be able to increase wages while preserving the company if we remove cheap, low wage foreign competition. I think that has been a root problem for awhile.

Why would you build your life around low interest rates? Historical rates are a Google away. If you levered up with zero room for rising rates, you were not responsible.

What's with all the people complaining about the rates? I'm appreciating earning 5% on my savings. There are two sides to every trade.

Without posting the details, was 13% that your parents paid a significant chunk of their joint earnings? This is the more important aspect of the current situation, not the percentage number itself.

I wasn't privy to too much of their financial details, but I know the rough price of the house. Assuming we were "average", based around average income for the year we moved there, it was about 40% of the average us income.

Huh. According to this post the payment-to-income ratio now is around where it was in the early 2000s, but is higher than in the 1990s. Both still significantly lower than the 40% your parents paid.

Well if my home price decreased in value by 20% that would probably give me roughly the same payment at a 7% interest rate (versus the 3.25% I currently have). The issue of course being that my house has slightly increased in value during the time that interest rates started to increase. When you combine those two things together if I bought my house today I would pay about $1,000 more a month for the same 3 bedroom house that I closed on not even 2 years ago.

Depends on how you define "normal". My parents had a 4 7/8% mortgage on a house they bought in 1966. (The only difference is that they had a prepayment penalty. The 1970s and 80s taught lenders why they shouldn't put that in.)

So, depending on your time frame, the 70s and 80s were abnormally high, post-2008 was abnormally low, and 5%-ish is "normal". (I think, if you keep going back, 5% continues to be kind of normal, but I don't have the data in front of me.)

I think the housing market has been too variable over the timespan when it has really existed (~100 years) for there to even be a "normal". I do think your guess of 5% for the short-term future is probably not too crazy though.

The long-term historical baseline interest rate for any kind of debt is 6%. I tend to see it as normal too, though may go high for a while in reaction to the artificially low rate of the last decade. Home prices relative to household income are high though.

Probably the end of a fixed interest period approaching. This is the case for some %age of the total number of mortgages out there every year. It's also the moment you're going to be taken advantage of.

Taken advantage of because you have to deal with them. Previously you had the option to walk away. But when the fixed interest term expires you are going to have to make some kind of deal because very few people can switch to being homeless or paying off their entire mortgage at the drop of a hat.

Presumably a 10/30 loan or something similar. Many homeowners are facing the same problem with the interest rate now being significantly higher than when they got a 10/30 initially.

Yeah, the US is an outlier. In most countries the government doesn't back mortgage loans so we have to refinance after a few years. Basically every mortgage in countries like Canada and the UK is what the US would consider an "ARM".

It's always amazing to me that people will write these long articles and then do things like compare real median income (adjusted to account for the price of housing) with nominal rent prices.

For context, here's nominal rent vs. nominal income, both indexed to 1985.

EDIT: Some criticisms of the charts the author uses:

1) The Case Schiller chart is in I guess "units"? The underlying data is an index to 2000, so saying it dropped '50' (going from 180% of 2000 to 130% of 2000) is for the most part meaningless. The farther you get from the year 2000, the bigger the numbers will look.

5) There's a lot of complex policy debate about whether or not we are in secular demand crisis, but the MBS chart is all about lowering interest rates to increase demand. I agree that has unintended consequences, but the author seems to forget that builders pay interest rates too.

For me it was the chart for investor house purchases. It's not shocking that investors are not excited to purchase properties with 7% interest rates when returns on investment properties are less than 7% usually.

with the caveat that we don't know what the bottom blue line looks like to date, from your nominal/nominal chart being in a bubble seems pretty plausible (assuming we call the 2006-2008 deflection a bubble)

But what about your property value? What about your net worth? Or are you one of those radicals who own a home to —*shudders*— live in it, rather than for its natural purpose as a financial investment?

My property value in the SF Bay Area was reassessed for $700k lower than my purchase price. Sucks but it means my property tax dropped by over 20% and I also won't leave my house since my interest rate is 2.6%.

Your comment is sarcastic, but the reason home owners love the bubble is because they can borrow money against their house instead of working for a living. So if you were lucky in real estate you can slack off at an easy job while making your minimum mortgage payments and live a comfortable life on borrowed money, maybe get a new car and a nice vacation?

Or if you're ambitious you borrow money against the house to renovate it and build it larger. Slack off at an easy job and you have energy to do renovations in the evening.

Every 10 dollars borrowed to do renovations becomes at least 20 dollars in increased home value when the renovations are finished, and as a bonus you get to live in the newly renovated house. You don't need to sell, instead take out another loan against your now more valuable house - the bank is eager to help. It's called a "real estate career".

Compare that to working for a living as your "career": Every 10 dollars of productivity you put in for your boss turns to 7 dollars in wages and after taxes you have 4 dollars. Not to mention the taxes and tributes as a small business owner or independent.

Which is the smart move? Which is the fool's move?

If you talk to everyday people, what is their dream? What would they like to achieve? Will they say they want to invent something? Create a huge business? Become best in the world or at least in their region in some sport or hobby? Very few will answer this. Most will answer: "I want to own a bunch of condos and live on the rent". That is the dream.

America is one of those places so alienated from the fulfillment and joy of providing value to society through work that almost everyone wishes on the parasitic dream of just living without doing nothing.

No it won’t. This reads of straight fantasy. The idea that an extreme minority is going to panic the majority into selling at bargain basement prices is absurd. It’s far more likely that either

1. People simply choose not to sell their houses; as most people who own one or more homes have that option, or

2. The 64% of people buy the homes selling for cheap, and resell for a profit

My (very limited, admittedly) observation is that people who own multiple properties do not panic-react to the market changes. A great example of that is London, where a vast number of houses and flats are unoccupied and that doesn't seem to bother the very affluent class owning the properties.

Agreed. Largely because they have the capital to hold on to the property, and also for as long has anyone has been alive, in most places owning a house has been either a safe or unbelievably lucrative investment.

The notion of lots of empty houses and flats in London is severely exaggerated. Sure, there are some tiny areas where lots of owners are people who have multiple homes, and so spends little time each place. But most of London haven't got that much empty space.

The London rental market is if anything completely overheating at the moment due to lack of supply.

Both West London and (surprisingly) East London had many unoccupied houses a few years back. Even in areas around Hackney road / Bethnal Green, which I would guess are not even really investment properties but more like long-term wealth assets.

Agreed on the overheated market. My argument was that these properties are completely off the market and the owners won't panic-sell them

London is generally nowhere near the top of the list of places with empty housing in the UK. It's "many" only because of the relative density.

As of April 2022, only about 34k properties were classed as long term vacant in London out of around 3.7m housing units, with Southwark, Newham and Barnet at the top of the lists, largely because of redevelopment projects that meant clearing out tenants first, as well as time to get people into new developments afterwards.

<1% empty housing is not unusually high for an area experiencing a lot of renewing and new builds.

I think the main difference is that, at least in the US, a lot of people that bought multiple homes in the last few years are fairly heavily leveraged. It's not "very affluent class owning the properties", but people that took out a another mortgage because they thought real estate was a sure bet.

The real issue in the US is going to come down to how many people can continue to afford multiple homes which is where rising interest rates and inflation both come into play. Anyone that bought a second home using an ARM may be forced into paying much more than they thought, and rising interest rates are going to put additional pressure on people with investment properties as they may need more liquidity sooner than originally expected to cover routine expenses.

> Except those who feel that prices will go down further and don't want to be left holding the bag. It's a classic prisoner's dilemma.

It’s not. The current mantra is that if prices go down, on a timescale of like 10-20 years they will eventually go back up. This is the way things have gone for at least the last century. AirBnB can go bankrupt tomorrow and wit will do exactly nothing to dispel this thought.

> With the current interests rates, this is straight up magical thinking.

Do you think that matters even the slightest bit? A nontrivial proportion of homeowners could afford to buy second homes outright at this point.

> It’s not. The current mantra is that if prices go down, on a timescale of like 10-20 years they will eventually go back up. This is the way things have gone for at least the last century. AirBnB can go bankrupt tomorrow and wit will do exactly nothing to dispel this thought.

If you are a hedge fund manager, and are considering pulling your money from a reit or not, I can assure you the "20 years" timeline is not anything you care about.

> Do you think that matters even the slightest bit? A nontrivial proportion of homeowners could afford to buy second homes outright at this point.

Doesn't mean they will be wanting to act as the greater fool with their savings.

> You're going to sit on a distressed asset for 20 years hoping it recovers? Do you realize how financially debilitating that is?

I’m saying they have the financial ability to do so if necessary. Approximately no one actually believes that the housing market is going to undergo a >20 year downturn because of AirBnB.

The trillion dollar question is what will actually make people believe the market is going to turn over for the long term. Because that’s literally the only way the markets are going to return to normalcy. And it’s not going to be because of some hotel app.

The market needs inventory for prices to adjust. With the "high" interest rates (really more like historically normal), home owners with a 3% mortgage don't want to sell, since they'll be trading their 3% loan for a 7% loan. So even though there are not a lot of buyers, there are not a lot of sellers either, so there is no pressure to reduce prices. Perhaps the the air bnb owners selling will provide enough inventory to let the shortage of buyers drive down prices...

"Her sun-burnished

skin was smooth and healthy, her eyebrows were straight and fine, and her teak-colored eyes

intelligent and quick. There’s an attractiveness unique to mixed blood and she had it, perhaps a

quarter of this and the rest of that.

For our first meeting she’d chosen to wear a plain black halter blouse that showed her

figure and bare shoulders to good effect and a peasant-style skirt of multi-colored, mixed-

texture fabrics. Her dark cascade of hair was pinned up in a chignon, revealing her graceful

neck. Her smile revealed even white teeth. She had the glow of the well-off and an unself-

conscious confidence. She was poised, slightly shy and visibly curious about me.

>The idea that an extreme minority is going to panic the majority into selling at bargain basement prices is absurd

While I have no clue how the housing market is going to turn out, I'd point out that edge conditions control prices quite often. When demand is higher than supply prices can increase very quickly, and the converse is true also.

I don’t doubt that fact, but housing isn’t a typical market. It’s a market that for most people’s lives, has never gone down for a long period of time. It’s a market that the government will actively intervene in to prevent it from going down.

If you talk to a lot of older Americans, a non-trivial portion of whom are invested in the housing market, their faith in the continued growth of the housing sector is akin to their faith in God. They’d rather sell their kidney than their second homes at a loss.

You would have to do a lot to get them to believe that the housing market is over.

As long as new supply is not being built, whether due to restrictive zoning, NIMBYism, or other such reasons, the bubble will not burst. Too many people simply want too few homes. The answer is to build high density housing in the places people want to live in, usually major cities.

Which will not happen because of the NIMBYism you describe. Local and state governments tend to have a high representation of property owners relative to the folks who really need this change to happen. It's "F you got mine" applied to housing policy.

Also tragic is people without homes fighting a proxy war with “developers” because of their podcast centric understanding of economics. It’s more important that developers don’t make a profit than increasing the supply of homes and nothing will change their minds.

If new housing supply has the word “luxury” in the name then lord help you. Gentrifying a community with new houses is like the worst thing a person could do.

It’s not true (at least not for the past 20 years nationwide). New housing has grown faster than population growth. In 2000 there were 113 units per capita vs 145 per capita today.[0] The average number of people per household hasn’t changed significantly since then, so there is technically 30% more housing available in the US than 20 years ago.

Not all of that housing is where people want it, investors are collecting properties like Pokémon, the vast majority of people can only afford a house half the price they could before interests rates rose, and those with mortgages are stuck with their low rates and little incentive to move (or at least sell).

So it’s not the lack of units that’s the issue, but a market that (surprise!) favors the wealthy and entrenched. If you had cash, houses could be found at absurdly low prices 12 years ago. But as always, the climate favored the wealthy whose credit score wasn’t wrecked, who had excess capital to deploy, and were willing to tie it up in real estate for 5-10 years as the market recovered.

There is a deficit of around 40 million units in the US.

Desired household sizes keep decreasing due to ongoing drops in marriage and childbearing rates, which increases housing units out of historical proportions.

This is compounded by the desire for vacation homes and the continuing opposition to increased housing in privileged areas such as the coastal cities.

Well a lot of people who want homes are expecting to be getting short-term rental revenue that would cover their mortgage payments at least. If they fail to do that then they might not want the home.

This is in turn dramatically impacts the price of the home.

I bought a home last year during peak sales season in a great neighborhood in a major tourist town at a very reasonable price that had been on the market nearly a week before I made my offer. How? Because my HOA explicitly forbids me from using the home as a STVR, which kept most interested buyers away. The desire to capitalize the house in the future is a major factor in rising home prices. I can do a long term rental, but no Airbnb.

Want to dramatically reduce upward pressure? Start passing laws that severely punish STVR activity and prices will come down.

Population increase brings job-opportunity increase. Then we will need even more high density housing. This is a vicious cycle. "Just build more housing" is not the solution.

Sounds like that's exactly the solution. Build more housing until supply meets demand, even if demand rises. It's not as if the population is infinite.

Why would it? It doesn't happen today even in countries with cheap housing, like internal migration in Japan. People aren't going to suddenly flock to countries for cheap housing, otherwise we'd see a bunch of Americans moving to Thailand or something.

Exactly, nobody flocks to housing on its own: people migrate to job opportunities. Which increase with population density. If you increase housing where there is already demand due to job opportunities, then you increase density there, and then you increase the job opportunities again, and thus you increase the demand even more than what you satisfied with the new housing.

I don't think you understand what I'm saying. The cycle you're talking about is not an infinite process, nor is it guaranteed that people will flock somewhere just because there is more housing, because it is also not guaranteed that job opportunities increase due to lowered housing. You have your causality incorrect there.

It's obviously not infinite because, as I said, there is a physical ceiling to how much housing you can cram into an area until it's too expensive. When you reach that ceiling you did not improve anything, on the contrary.

Okay, you cram as much housing as you want in an area, then what? Just because you build X number of houses does not mean that X number of people will move there. That is what I'm saying, your order of cause and effect is reversed.

I suspect you haven't been to Thailand, cuz there is a shit ton of expats hanging out there. Laws about visas and home ownership -- can't own a house unless you're Thai -- complicate that.

I have indeed been to Thailand as well as a lot of Asia. My point is that as many expats are there, most people in the US aren't going to go to another random country simply because there are lower housing costs. While housing costs are correlated with movement of people, there are many other complex factors involved.

Real estate prices have been increasing more than any asset for decades in regions that have catastrophic depopulation. There is no shortage of housing. Abandoned houses are everywhere, I've seen them rot before my eyes through the years. Abandoned land is everywhere, I see it overgrown. Ask to purchase that abandoned property and you'll be hit with an outrageous price demanded.

Is it sound to organize your economy in a way where the mere luck of owning real estate will net you the same income as what a specialized professional has to work decades to earn?

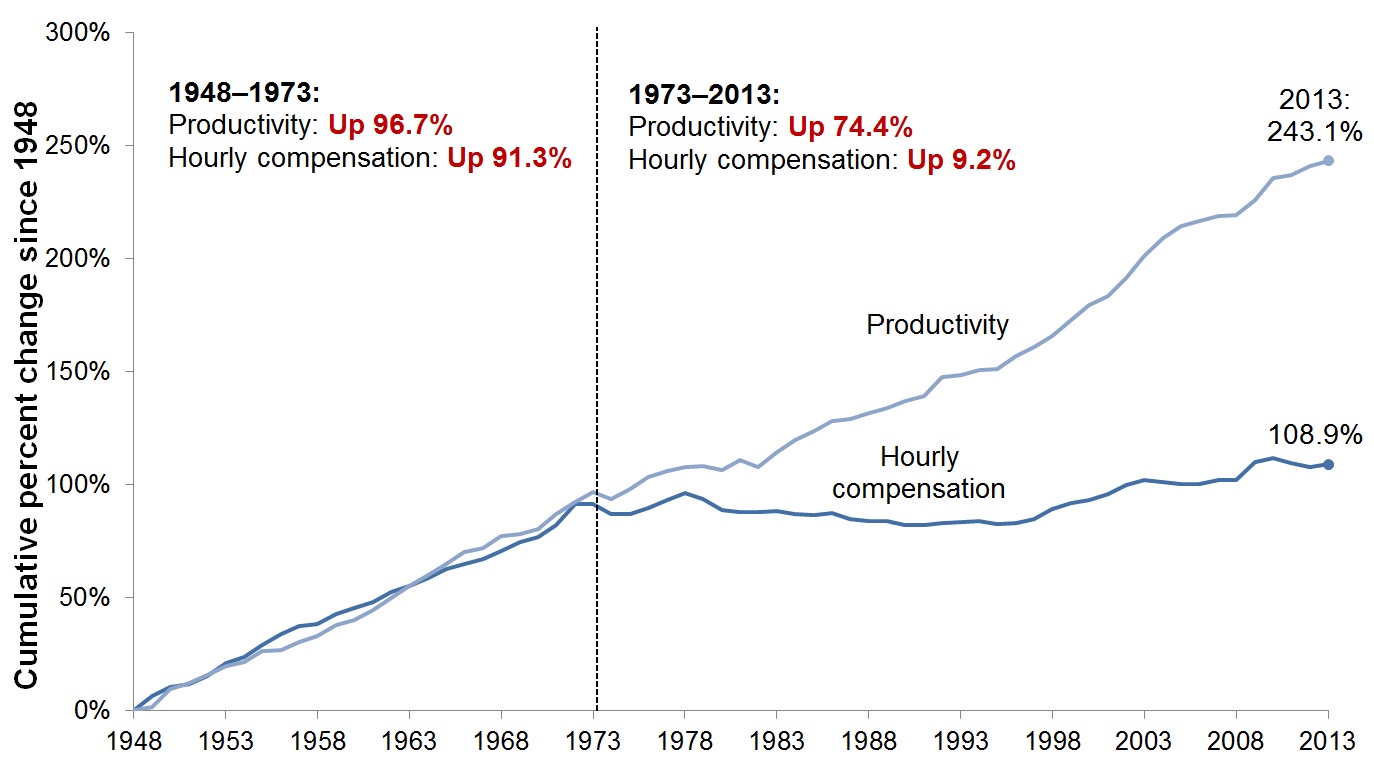

Consider that the market is no longer the 90%. Since real wages have not risen much since ~1980 [1], most of the consumers have no response when rates suddenly increase. Houses are simply not purchasable.

Case study: Vancouver, BC, Canada (I looked in May 2023). House prices: ~$1.1M. Loan rate: ~5%. Month payment: $5900. Yearly: $71k. Avg Salary: 60k (before tax). Result: No normal worker can afford the loan, and the bank won't give you the loan.

When interest rates sharply rise, suddenly all loans to normal humans based on existing prices look like failure, because there is no way to make the payments. "I'll give you a loan, so you can miss payments every month, owe me more every year, and then default. No." if( money_earned < monthly_payment) then { no_loan }

Also, wealthy need somewhere to park their money. A bunch of really wealth folks made a bunch of enormous profits last year. [2] Frankly, if you're in the $10^9 club, there's not much to buy. Personal air craft carrier? Your own airforce? Build your own town? [3] Reconstruct all of Iraq? [4]

Vancouver, especially, has not seen salary gains in keeping up with the housing market. It is explicitly, unambiguously, huge amounts of foreign money. The housing prices in greater YVR correlate to foreign issues in China like Xi's crackdowns, or MBS' takeover in Saudi.

This is true for Greater Toronto as well, but very much less so over the rest of Canada.

It's not uncommon to visit tourist-magnet cities and see entire buildings with only a few lights on, as many units are owned by the wealthy and left empty, as rents are not as important as having a safe place to "park surplus capital." Thousands of other units have been pulled from the long-term rental market to reap the higher returns of STVRs [short term vacation rentals].

In NYC, another sign of STVR buildings are lockboxes chained to metal railings outside.

Starting tomorrow (September 5) such rentals are supposed to follow very strict new rules introduced by the Adams administration including hosts required to live in the same unit and reservation caps of no more than 2 people. Whole apartment rentals are banned unless the term is longer than 30 days.

Haven't heard of this change! Thanks for posting. Curious to see how this will affect the STVR market (even just the number of postings and their availability on AirBnb).

Someone mentioned in this thread that a likely scenario is these landlords switching to mid- or long-term rentals instead of selling. Which sounds very plausible to me, especially in a city like NYC, where the rental market is always hot.

> It's not uncommon to visit tourist-magnet cities and see entire buildings with only a few lights on, as many units are owned by the wealthy and left empty

Talk is cheap. Show me the maths. NYC has a vacancy rate of ~3%. That's the lowest in the country.

Are you referring to someone declaring a condo as their primary residence and not using it as such? Or are you saying that all condos do not count towards the vacancy rate?

If there is lots of evidence for the former; it should be shown.

My comment was definitely flippant but in large metro areas airbnb at the margin leading to a rapid price increase is not the problem. It’s supply. No supporting evidence here because it’s pretty broadly available for many real estate markets.

If there is suddenly 5x the supply from airbnb divestment, it can move prices. It seems like the winning move is probably to just do a regular rental instead of selling though.

Housing is different than other kinds of assets because it is also essential for nearly everyone to have a home. Most people in the market for a home only have their paychecks and credit from the bank. Median wages are quite a bit lower than FANG salaries and banks only give credit to people with appropriate incomes buying appropriately priced homes. Governments also need to keep people in housing and voters will kick out any government that fails too hard at that.

So unlike bitcoin, housing cannot stay irrational and divorced from fundamentals forever. Real people need to use real paychecks and actual local credit unions need to look at those purchases and see a safe bet.

If that system stays out of whack for too long, everything collapses, the banks’ business model, the housing market’s prices, the ruling party’s majority, rule of law as the people resort to squatting and the capitalist system that failed in the simple task of keeping people out of the rain and cold.

Considering most of those houses in question here were bought at 3% interest rates it seems unlikely that the wealthy would sell at a loss rather than just switch from STVR to medium-term or long term rentals where they would make less money. The housing market is still short on supply and at the purchase prices/ interest rate combo they have a lot of room to be able to ride it out.

Besides, its not residential homes that are a ticking time bomb, its commercial properties... Office workers are not going back to the office.

There are all sorts of renter protections that come into play once you are no longer a short term vacationer. I think these protections will turn “investors” off.

>>Office workers are not going back to the office.

I am not seeing this. Major companies are forcing the issue, and employee can pound their refusal all they want but at the end of the day I think we not going to see a normal fully remote work force.

At best you are going to see a hybrid where you get 2 or 3 days a week of WFH, and the balance in the office.

Further from personal experience I somewhat agree with the management because I have seen LOTS of abuse of WFH from employees.

At first I was concerned about abuse of WFH by employees too, but then I realised, people in the office often aren't particularly productive either.

From my own team, if I had to guess, the actual number of productive hours are similar.

Granted, I think it probably varies dramatically by company / team, and I get the impression that some places take WFH much less seriously than we do (as in, not goofing off).

Absolutely. Everyone in my office is pretty considerate, but all it takes is one pair of people in the bullpen and the quiet is gone. We all get to listen to the discussion. When I first joined, I learned a ton by eavesdropping. Now it just stops my workflow by distracting me. I'm easily 10 times more productive at home.

For us it varies dramatically by team, but the problem is a WFH policy needs to be company wide for the most part. All it takes is for a few teams to cause a problem for everyone.

>>people in the office often aren't particularly productive either.

Some of that depends on how you define "productive", having non-work related conversations while in the work place may not be "productive" but it is team building

Watching netflix, or doing your laundry when you should be working on a report is neither team building or "productive"

Further lots of informal conversations are how many many many many business decisions are made, and how lots of information flows through a company.

So many times I have been made aware of new projects, changes, or other things happening in the company simply because I happened to see someone in the hall and they happen to mention it... That would never happen on a formal call. meeting, etc in a fully remote environment.

Those hallway conversations are less productive compared to someone doing laundry while thinking about how they will approach issues.

Those hallway conversations are wasted time. You should be at your desk doing your assigned working not socializing. Corporate team building is a guided exercise run by experts not doing work hours

Informal meetings exclude stakeholders and don't allow for documentation. Informal meetings are duct tape over process issues.

This is it. I’ve actually found it’s down to the discipline, like our tech team is fully remote and that works super well even though the sales team is in-office.

Not only is our tech team fully remote, we’re spread out in the US so there’s no small part of our team that’s more often meeting up in person to work.

Work from office is absurdly expensive for society.

5/7 of the days, relocating an entire city worth of knowledge workers across town to a computer screen is fairly nonsensical.

You force everyone to live within a radius of economic hubs if they want job mobility, or you have to be comfortable relocating your family every N years for upward mobility in your career (or take the career hit, wait for internal promotions, and risk the company folding).

It’s socially not great. It’s economically not great. It’s environmentally not great. Working from the office is just all around not great.

Speaking personally, I live in a good community, with a good quality of life, a good school district, I can afford a good home here, and I can provide for my family. I’ve setup roots and intend to raise my kids to adulthood in this house.

I’d be surprised if anyone could afford a competitive package that would convince me to relocate my family, pulling my kids out of school, selling my home, and paying the toll of a daily commute.

The rest of my career is remote. Companies can do hybrid. They can return to office. They can do whatever they want. Unless they support full remote, I’m not part of their talent pool.

I know many people who think this way. And that number is growing.

Yeah it’s plain silly. As a remote worker for going on 3 years, I can’t ever see myself going back to a commute. You could double my salary and I wouldn’t do it..

Yep, I don't care what they do. I've been remote for 7 years now, I made it work before COVID, now it's like playing on super easy mode.

My Dad was a work from home pioneer, from back in the early 90's. We got all the latest modem and other tech growing up. If he could make it work with a 2400 baud modem, we can make it work for pretty much every office job.

>>I’m not part of their talent pool. .. I know many people who think this way. And that number is growing.

you enjoy that freedom due to low unemployment, and stable(ish) economy currently.

Unfortunately the fundamentals of the economy are not sound right now, and very likely we will start seeing companies fold, and unemployment numbers go up.

It is very easy to have a hard stance on fully remote when you have 2 jobs for every employee on the market... if that flips I have a feeling peoples demands will change.

> Work from office is absurdly expensive for society.

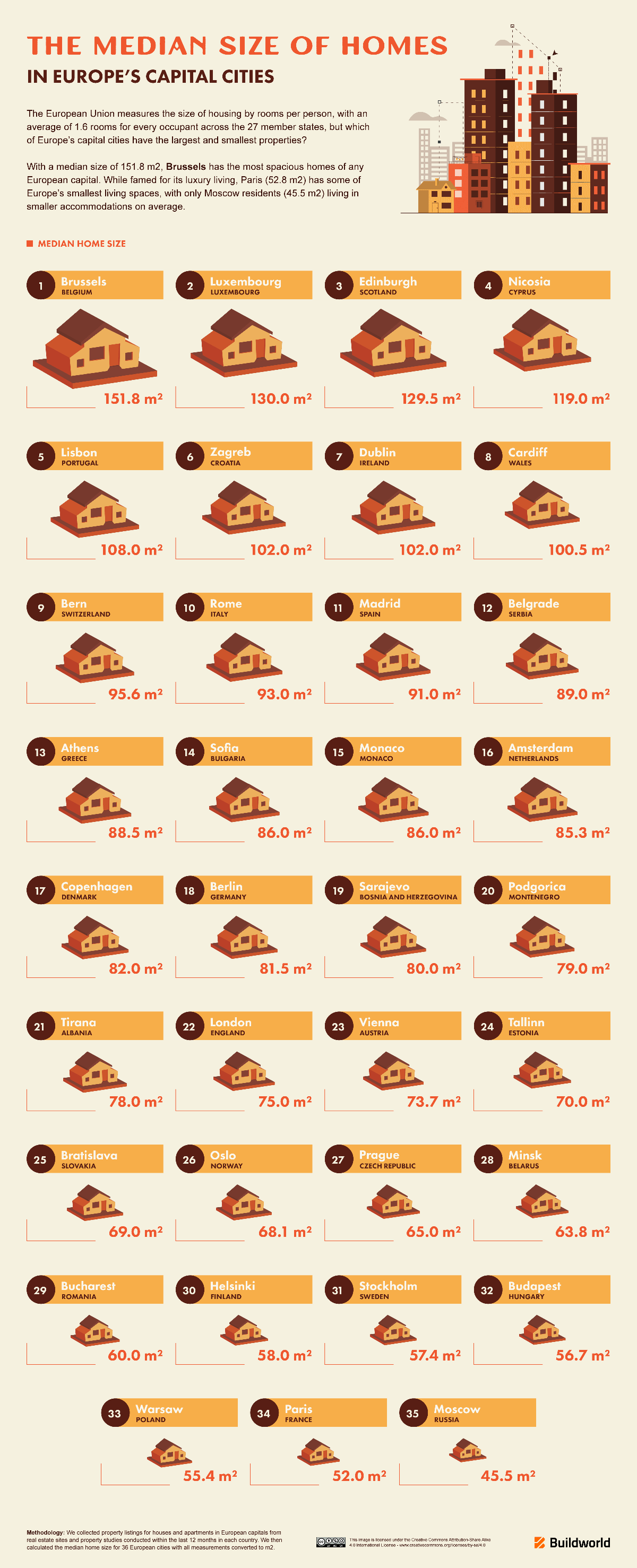

That assumes everyone lives in American suburbia with one extra room for your home-office. Guess what, most of the knowledge workers live in dense cities with tiny apartments. Average flat sizes for various cities (sqft): Bangalore (1260), Singapore (667), Tokyo (710), Paris (520) etc. See this image for more details: https://files.buildworld.co.uk/average-home-size/03_Average-...

To make it permanent remote would involve a huge restructuring of those societies and that cost is much greater than maintaining office towers.

Who the hell is trying to work remotely from their shoebox apartment? That's the point of WFH -- you can move out of Tokyo to rural Japan and live in a larger space for cheaper. Or rural France. Plenty of space in rural India.

Not much luck for Singapore tho, but that's the nature of the city-state.

> To make it permanent remote would involve a huge restructuring of those societies and that cost is much greater than maintaining office towers.

bollocks. MS Teams or Slack is cheap, and the cost of moving to a rural locale isn't hard. Smaller towns will develop their own amenities, and 2nd and 3rd tier cities would do well.

But I have been told for a very long time that no one actually wants to live in a rural space, that people are just forced to do so because of cost, or some other such thing..

or that people that live in rural spaces should not be allowed that because it harms the eviroment or something.

I have had many many many conversations where people tell about how wonderful urban life is, as how that is the best way for people to live, in shoeboxes where everything is in walking distance from them...

seems WFH is in direct odds with the "walkable cities" movement

It seems you don't have any family and friends near where you live? Or you don't have any hobbies which are possible only in the cities (eg. being a foodie with a taste for various types of cuisines)? Or you are a native born who will find it easier to blend into rural communities who are typically more homogeneous? Unless you can only see costs in financial terms but not in social or personal terms?

Cost of urban to rural transition is HUGE, first at individual level due to social ties and personal preferences. And then at societal level due to personal preferences of the electorate. Dense cities are here to stay in most of the world.

The lack of empathy in your comment is surprising.

I’ve lived in quite a few places across the size spectrum. I’ve lived in big cities, small cities, suburbs, and small towns.

In all of those places I’ve seen strong communities and social isolation. I’ve seen opportunity and poverty.

Your painting of rural life, small city life, suburban life, etc. is unfair.

Cities have a lot to offer that rural life can not compete with. Rural life has a lot to offer that cities can not compete with. So does everything in between.

For that reason, I suspect you are correct that dense cities are here to stay. I also suspect that small cities, rural communities, and suburbs are here to stay.

The deciding factor here is if the owner can find a cash flow source that covers the mortgage payment, property tax, and maintenance costs. NYC lease rates have surged since the state revamped rent control laws.

> it seems unlikely that the wealthy would sell at a loss rather than just switch from STVR to medium-term or long term rentals where they would make less money

isn't that the point?

force these to be rented in med to long term, or at least 1 year leases, so to open up the housing market for people who want to, like, live somewhere.

I see a lot of Airbnb-hate online like reddit or Twitter, but financially I see no sign of Airbnb slowing down at all. It really just seems like a case of more light and no heat at this point.

I think you mean STRs not AirBnB? STRs are still growing, but AirBnB is facing much more competition from VRBO and Booking.com and Google Travel then it has previously faced. When I consulted at https://futurestay.com I could see the income shifting from AirBnB to Booking.com.

I understand your point, and it is a heuristic at best, but I'm having more and more trouble listening to the ever-growing gymnastics explaining how prices will not come down even though mortgage rates have gone from 2.75% to 7+% in the last year-and-a-half.

I have yet to hear a convincing argument beyond "people will just stop selling their homes, forever," which is obvious nonsense. Once the adjustable-rate mortgages reset in a year-or-five, many, many folks will be forced to sell. Prices only come down when people are forced to sell at a loss.

Decreasing in real value, sure, but people hate the idea of a nominal loss when it comes to selling their house. And with inflation still higher than usual, it's entirely possible to have a 15-25% loss over five years in real terms while still looking like a wash on paper. That seems like a more likely scenario than an outright crash right now.

STRs are still a small fraction of the total housing market, as are institutional investors. People need houses, this market is organic, though reacting to the massive flux in interest rates.

A key argument appears to be based on incorrect data.

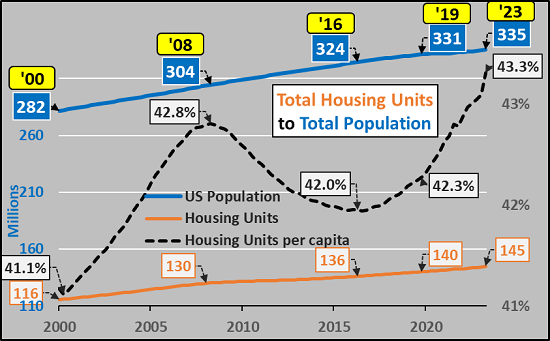

Specifically, as I write this, the OP states that the number of housing units per capita in the US is at an all-time high, per this plot (unless the OP changes it):

> I also want to stipulate that I am not talking about people of modest means who acquired rental properties by scrimping and saving their earned income and making sacrifices for decades--a strategy that is part of Self-Reliance ; I'm talking about the already-wealthy who are seeking to "maximize returns" on their unearned "surplus capital."

The mental gymnastics folks go through to say "this behavior is ok if people I like do it, but it's wrong when those other gross people do it" always amuses me.

In stories like this, I think that sort of thing is less about mental gymnastics, and more about picking a less controversial target to make their point with.

While I cede your point to an extent, small time landlords are generally (1) small, local businesses, giving back to the local economy, and (2) very motivated to keep the places rented rather than sit idle. Which is to say at least somewhat invested in the community.

I 100% agree, but the difference you are pointing out relates to how a landlord acts and works with the community, not how they became a landlord in the first place. There are plenty of "small time landlords" who simply inherited a house when their parents passed away and chose to keep it to rent out. The author of the article is implying we should demonize these small time landlords because they didn't "scrimp and save their earned income over decades" (even though their parents did).

I agree with this. Emotional investment is entangled with a generational home. You don’t want an inherited home with positive memories to turn into a drug den, so you’re incentivized to screen out unfavorable tenants.

If you’re a large-scale real estate corp, the houses are just income earners and as long as the income is greater than the n expenses, you don’t give a rats ass who lives there.

Well, he does have a point. Someone investing their life's savings to buy a second home for rental income is not the same as someone like Infy's Shibulal buying 700+ homes in Seattle [1]

> A systemic driver of this bidding war for rental properties is the "AirBnB" model of monetizing individual properties to compete with hotels and resorts for lodging... This has led to an artificial scarcity of housing in popular tourist destinations.

This is fundamentally untrue, there is nothing "artificial" whatsoever.

AirBNB allows a city to host a larger number of tourists than hotels alone can provide, which stimulates the local economy with lots of spending etc. This is not "artificial", it's real local economic growth.

The scarcity of housing is then not caused by AirBNB -- it's caused by not constructing enough housing.

It doesn't matter whether demand for new housing comes from tourism or people moving to the city to reside. Demand is demand, and tourism is not "artificial". Nobody calls people moving to the city for work an "artificial" cause of scarcity, and neither is tourism.

This assumes the owners of the STVR units are local. My guess is the longer the phenomenon goes unregulated the more they're owned by distant rent seekers.

If you're making a comparison, then you're assuming the owners of long-term residential buildings are local as well -- which they most certainly are not always. And I don't know why STVR owners would be less likely to be local than regular landlords. (And then if want to send money to hotels, remember those are almost always national chains!)

But in any case no -- I'm talking primarily about the fact that tourists spend more on restaurants and attractions and shopping than locals. While I'm assuming that landlords just remain landlords.

No it doesn't in most of the places we're talking about, that's the whole point.

Most places aren't Venice, built on islands with nowhere to expand, and wanting to preserve their ancient architecture. And NYC, where AirBNB is about to be massively reduced, doesn't have any risk of being hollowed out into a shell.

Most places should just build more housing. Then locals aren't priced out at all. That's just supply and demand, basic economics.

> AirBNB allows a city to host a larger number of tourists than hotels alone can provide, which stimulates the local economy with lots of spending etc. This is not "artificial", it's real local economic growth.

I live in a tourist city - there's no shortage of hotel rooms. As tourists flood into livable dwellings, hotel vacancy rates have skyrocketed, and rents for the locals are skyrocketing as well.

Usually tourist cities don't have a hard time building new hotels. Building new housing can be tough. Hotel taxes are popular with the locals for obvious reasons. Property taxes aren't. NINBYs don't like residential density either.

For better or for worse, the only way out of this is through regulation.

> I live in a tourist city - there's no shortage of hotel rooms.

How do you know?

It's not going to show up as hotels always 100% full.

If there was demand from 10,000 tourists, and there were 7,000 hotel rooms and 7,000 AirBNB properties, then you could have 5,000 (71%) of hotel rooms occupied and 5,000 (71%) of AirBNB properties occupied and you'd think there was no shortage of hotel rooms.

But there'd be no shortage of hotel rooms only because of AirBNB. The reality is that there'd be demand from 10,000 tourists and only 7,000 hotel rooms.

> Usually tourist cities don't have a hard time building new hotels. Building new housing can be tough.

Well tough on them. Lots of things are tough. I have no sympathy -- new housing should be built, end of story. It's not sending a man to a moon, it's just regular old governance.

It's very clear that many tourists want to stay in AirBNB's. This is a valid consumer preference to stay somewhere that feels more like a home, in a place that feels like a neighborhood instead of a busy downtown, with a normal amount of space rather than a cramped hotel room, and at less cost. It seems silly to say that's a bad thing.

> It's very clear that many tourists want to stay in AirBNB's. This is a valid consumer preference

Well sure it's a valid preference (I'm not sure what an invalid consumer preference looks like), but city governments will (and should!) obviously prioritize the needs of residents over the wants of tourists. Residents want to live in the houses that are currently sitting vacant 4-5 days of the week, and completely empty through large swaths of the winter. It's horribly inefficient. Residents want tourists to stay in hotels, not drunkenly partying every weekend in their own neighborhoods. Residents don't want their rent to keep rising 3x faster than their wages.

It will be frustrating to some tourists and the folks sitting on short term rental empires, but the tourists don't get to vote on these issues and the Airbnb investor gurus are outnumbered.

In the coming years Airbnbs are going to get severely restricted, regulated, and taxed in every major metropolitan area that has both tourism and a housing shortage, because it's such an easy popular thing to do.

Has this guy ever been right? I just remember him writing about the coming housing crash for the last 15 years. It never manifested itself and just kept going up. He has never been correct in his predictions, so I would actually use him as a contrarian signal.

Hah. I came here to post the same thing. He's definitely a permabear. I like some of his insights, but in the past he and his circle of friends have rarely been right. (Of course when they were, they were really right.)

1/100 UK properties is an (Airbnb) short let of some sort. But I don't buy that a few highly-leveraged people panic-selling their portfolios is going to bring down house prices at all.

Even if that caused some _local_ downward pressure on house prices, why would that affect the demand for short lets? It might reduce the supply, so local room rates would go up. The remaining owners would have a lower-valued asset producing higher returns - a better return on a percentage basis, and in cash.

Few people holding cash-generating property will be pushed into selling by a dip; lots of them will have held through 2007-14. Property value as investment is (still) a bit of a religion here.

Councils and national regs have far more potential to dent Airbnb numbers (e.g. I'd guess we'll see sales tax added on nationally by the next government). But I don't see the political will anywhere yet, even in places like Edinburgh and London that have unusual regulation.

AirBnB is banned in many cities, and that doesn't make much of a difference. Urbanization is not slowing down, and that drives up prices if not enough housing is built.

Popular Tourist Destinations tend to be places that people do not just travel but move to.

> Here's how we can tell if a speculative bubble is a bubble: everyone says it isn't a bubble

What an incredible sentence. Is a speculative bubble a kind of bubble? But then there's no need to tell whether such a speculative bubble is in fact a bubble. Anyway, we can tell if everyone says it isn't a bubble. Cars are a bubble. Lolipops are a bubble. Everyone says these things aren't bubbles, which means they must be.

>At the budget meeting, elderly people were speaking up on how they cannot afford the tax increase.

Property taxes are the only taxes that, by definition, the owner of the property can afford. The elderly people only mean that they "can't afford" their property taxes without changing their lifestyle in any way. To be fair to them, it's certainly challenging and uncomfortable, however, this is a consequence of their own making. None of them were complaining during the 30 years of their property values were going up as supply became more and more stifled.

Cheers to that. IF the housing bubble pops, perhaps all the airbnb's revert back to actual long-term housing and the housing crisis / crazy rental market fixes itself. Capitalism, just fixing itself. Nothing to see here, no reason to worry.

Booking and airbnb pushing prices all over the planet

Ive been there I tried that

Now a days I a bring a tent cuz I love waking up on a beach or on a pastureland with cows on the country side in the morning.

You can also rent a cheap combi car and use it as a tent o vacation and go anywhere.

I think a lot of the economy/stock market has been juiced by people refinancing their homes as prices went up and using that money to buy second homes, new cars, remodel their homes, new phones, etc. Now that rates are higher, I think the rest of the economy will cool off as people can't use their homes as ATMs which will lead to a consumer spending slow down which will lead to a stock market correction which will lead to layoffs and finally start forcing more real estate transactions.

So on the topic of NYC, and the new registration laws coming into effect tomorrow. From Bloomberg:

"At stake is potentially millions of dollars in lost revenue for Airbnb in one of its biggest markets. Some 7,500 units don’t meet the requirements to apply for a license, according to market analytics firm AirDNA, and so will likely eventually disappear from the platform. More than half of those listings are frequently rented and account for about 40% of Airbnb’s income in New York City, according to AirDNA. In a lawsuit against the city over the rules, Airbnb said it earned $85 million in net revenue in 2022 in the Big Apple, which is about 1% of its total.

New York has been sparring with Airbnb for years over rules that prohibit rentals in most apartments for fewer than 30 days without a tenant present. AirDNA estimates that only 9,500 of Airbnb’s 23,000 listings are legal."

Will that few units (out of a city of 8.5M) coming back online really pop the housing bubble?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

investors should not be buying housing stock.

reply