i pay my rent and bills with wire transfer, same goes for 99% of my purchases ( mostly on amazon ) ... my paycheck is sent me as wire transfer as well ... how am I supposed to live just on cash? :) I only use cash to buy cigarettes basically XD

Though I don't think they mentions it in the article, I get the author is suspicious that the government may also inflate the value of their money away -- which it actually is.

"I do not accept their fees, they’re way too much high for the quality of service they give to you." So to fight this the author is paying Cashila.com/BitWage.com transaction fees and CryptoPay fees and takes on the exchange rate risk.

"I do not accept the concept of “trust”"

Right Cashila.com/BitWage.com are operated by magic trustworthy unicorns.

The difference is that with those services, you can always close your account and switch to a new one ( that's why I've specified to avoid using them as your primary wallet ) ... on the other hand, if a Bank goes bankruptcy, it's not that easy to recover your money.

Did you have more than $250,000 in your account? If so, then you would have lost access to part of your money, or gotten if after a bankruptcy court hearing. Deposits are not the highest priority item on a bank's liability side of the balance sheet, and as a depositor, you'll likely not get paid in full.

Ownership category is just something like single, joint, retirement, etc. If you have more than $250,000 spread across multiple accounts but with the same account holder and ownership category, the excess is not covered.

Totally agreed, I just didn't want any clueless HNers with lots of cash lying around trying to open a second account to secure their money on the basis of that comment.

Still, saying that you don't accept the concept of trust is a weird statement, especially given that the next sentence ("I don't trust them") uses it ;)

I think you still trust those services with your money in the same manner you trust classic banks - no real difference here, both can be used just for transfers and not keeping anything with them. Except for with banks it's really tiresome and inconvenient to load on demand and with Bitcoin it's nearly a one-tap experience.

I had money in a savings account at an FDIC-insured bank. It went under during the recent recession and there wasn't even a blip in my service -- all of the accounts were transparently migrated over to a new bank that the government had paid to take over the old accounts, while ensuring that all of the money that was supposed to be in those accounts actually was.

> I do not accept the concept of “trust”, I don’t know those guys, why should I trust them? On the other hand, with BTC trust is not even considered to be a factor.

This is a strange argument to me. There's plenty of community credit unions around. For trust you can walk right in and speak to the manager. Some of them are older than dirt.

However there's nothing really new in these fears (especially after 1929). The solution has always been to keep your money locked up in a safe. Pay for things in cash or cashiers check.

i pay my rent and bills with wire transfer, same goes for 99% of my purchases ( mostly on amazon ) ... my paycheck is sent me as wire transfer as well ... how am I supposed to live just on cash? :) I only use cash to buy cigarettes basically ... using only cash would make my life very, VERY, hard.

Here in Switzerland the entire financial system is arranged via wire transfers.

I get a bill. At the bottom of the bill is a red pay-in slip with a magic number on it. I log in to my bank, enter the number, tell it how much I want to transfer, done.

There's a not-used-enough automatic system where one of my creditors can send their bills directly to my bank. Now, I log into my bank, get told there's a pending e-bill, at which point I select it, press 'pay', done.

No fees anywhere.

I'm from the UK, which is just starting to do this, but it's nothing like as polished; small traders and tradesmen still prefer cheques, and regular payments are typically done via direct debit, where you authorise them to debit money directly out of your bank account (with a whole pile of banking guarantees). Switzerland seems to do this much less frequently; most people just pay the invoices monthly.

With wire-transfers you mean international wire-transfers?

I think it might be just an american thing, mexican banks usually don't charge you anything for wire-transfers inside the country (in their "use your credit/debit card at least once each month plans") and well, it's Mexico.

Though I think "first world"-something is quite the phrase just to describe consumer comfort: not advanced, not better (or worse), just "it's ok, I don't mind".

---EDIT---

Wire-transfers between national banks are free if you wait a day; there's a small fixed fee if you want them immediately. Transfers between different clients in the same bank are free and immediate. And it's becoming very common to be able to pay a quite assorted list of services through your e-bank account (from utilities to departmental store accounts) without fees.

It's not really a viable option for anyone. You're exposing yourself to huge risk of theft/destruction/confiscation, and you're losing out to inflation every year. Much safer to keep your money in an FDIC-insured bank account. If you have more than the maximum, then open up several bank accounts.

Any event catastrophic enough to wipe out money in FDIC-insured bank accounts would also affect your paper currency. If you're really worried about that eventuality, best to hoard gold.

EDIT: Let me clarify, I suppose it is a viable option if you are living paycheck to paycheck, but if you have accumulated wealth of any significance, it is not.

>I have to pay income tax, just because I receive money through bank account.

No, you have to pay income tax regardless of how you receive money. Bitcoin just makes it easier for you to avoid the law and be a leech on society by not paying taxes.

Ah, got it, so you're one of those people, one who heard the news about the Panama Papers, and rather than being outraged, thought "Oh that's a good idea!"

I don't know where you live, but here in the US the IRS simply has to ask you if you have a foreign (or crypto) bank account and you'd smart not to lie to them.

If they can't get the money because they don't have he private key they can simply put you in prison.

You haven't really thought your own question through very far, have you? You pay your internet and utility bills with cash? That's a problem in the U.S. In other countries many businesses are cashless, often even public transit is increasingly cashless.

Update: I'm even thinking of landlords of multitenant buildings, there's just no way they're going to take e.g. $100,000 in cash from everyone each month. It's really not workable. The apartment I had in NYC a few years ago was conventional check only. No cash possible, no credit card, no EFT.

Here in Brazil, ISP and other bills usually come in the form of a Boleto Bancário (https://en.wikipedia.org/wiki/Boleto_Banc%C3%A1rio), which you can pay with cash at the bank (or at lottery stores). Utility bills use a similar system. From the point of view of the bill issuer, it's cashless.

I don't know how it works on other countries, but I'd expect similar systems.

No, I'm thinking of the landlord making that size deposit. I know of no one walking around with $3000 cash to go pay rent let alone the landlord walking even two blocks to a bank to deposit that from everyone in the building.

> The solution has always been to keep your money locked up in a safe. Pay for things in cash or cashiers check.

You are never safe against the risk of fiat money devaluation, though (or even folks breaking into your home and stealing your safe).

Of course, the devaluation risk exists with BTC as well, but at least it does not depend on a central government.

BTC is almost worse - it depends on the whims of a totally unaccountable and often drama-filled group of developers who make decisions (or don't, in the case of the block size debacle) that impact the product as a whole. And if not them, the large mining cartels.

At least the fed has the bureaucracy and some manner of legal system keeping them in check!

Don't say "forks" either - we may or may not be at the point of maximum entrenchment yet, but requiring literally every BTC user in the world to update their software for their money to work is unrealistic.

I'm quickly coming to the conclusion that bitcoin is about as perfect a medium of exchange as you will ever get (immune to censorship, immune to legislation), but is comparatively awful as a store of value.

The United States Government is extremely likely to provide more stability.

The same cannot be said for every government, in fact the number of people that are under a government that forces them to use a currency that is more unstable than bitcoin is already in the 10s of millions.

If fiat money gets significantly devalued, you're going to have big problems no matter what you invest in or how much BTC you hold. Remember, deflation was one of the factors that made the Great Depression so hard to recover from.

There's also the risk of a redenomination. Bank accounts and other monetary instruments are automatically converted in that case; physical cash has to be brought to a bank to be exchanged, and there's often a time limit.

And there's also the risk that, as newer notes and coins come with stronger anti-counterfeiting measures, older notes and coins aren't accepted anymore, or accepted only with a discount over their nominal value. (I've seen it happen with older USA dollar bills left over from a trip to the USA a couple of decades before.)

My money's on, he hasn't reviewed all the lines of code in the Bitcoin client (or operating system, even!) he's running, either, so...trust comes back in a different form.

For my part, really, at the end of the day, I'd sooner trust institutions that have been around for a long, long time (far longer than I've been alive so far) than a coding project that's been around for less time than most of the popular websites I read.

But it'd be a funny old world if we were all alike, of course.

>For trust you can walk right in and speak to the manager.

His point with BTC was that you didn't even have to trust some manager.

>However there's nothing really new in these fears (especially after 1929). The solution has always been to keep your money locked up in a safe. Pay for things in cash or cashiers check.

I think he means to store the bulk of the cash on your own, and it wouldn't be inconsistent to store a couple thousand in a bank to access the usual banking infrastructure.

If you wanted to avoid even that amount of storage, you can also use them primarily for borrow money(credit cards, loans, mortgages, etc.) and pay the debts back with cash. I can access borrowed money through my bank's online interface.

Bitcoin involves trust in the mining community: human beings whose identities you almost certainly don't know.

Unless you are also auditing all the code you use for software that objects with Bitcoin yourself, it also requires trust in either the software developers or other people who purport to be auditing the code.

The idea that Bitcoin eliminates the need for trust is a dangerous delusion.

> Unless you are also auditing all the code you use for software that objects with Bitcoin yourself

As I mentioned in another reply, compared to existing electronic monetary systems, an open source one will always be more trustworthy than a closed source one.

>Bitcoin involves trust in the mining community

To be a part of Bitcoin, miners need to follow a publicly known protocol that is easily verifiable by anyone using math. Additionally, miners never have direct control of your money: they can't spend it on your behalf.

I think the only point you have there is that you must trust someone somewhere to mine Bitcoin. And as long as there's a profit to be made, someone probably will.

All you are doing is arguing reasons why the people you need to trust to use bitcoin deserve that trust, in your opinion, which is very different than the idea that bitcoin eliminates the need for trust.

The more reputation they have, the more that reputation is worth in business and the smaller chance they have of it being worth it to steal your money. older would typically mean more reputation.

I up-voted this because it is an interesting guide in securing bitcoin.

I think this is stupid in the extreme, and you SHOULD NOT do this ever.

Bitcoin is super interesting as an asset vehicle, but I would not put all my eggs in that basket. For as much as I might not like the Fed and some of the monetary policy it makes, it still gets things done. Right now bitcoin can't seem to change the block size, it needs to, and a squabble could cause serious devaluation of the product as a whole.

There is also the ticking time bomb of the satoshi coins. Right now one individual (or group) controls something like 6% of all the coins available, and on a whim, could cause a major devaluation over night.

All this having been said would I consider buying and holding some bitcoin as very LIQUID asset, and cash equivalent. I sure would. How much would I put into it, no more than a few grand honestly, a sum I am willing to loose.

The Fed, like all public institutions, is ultimately answerable to every voter. It's one of the benefits of citizenship, the decision-making power is in our hands.

No, your one vote won't change everything to suit your personal preferences, and if you wanted to change the way some aspect of our system works (like money, or health care, or drug policy, or whatever) it'd be a lot of work, consensus-building, and time. But, at least the power is in our hands, collectively.

The Federal Reserve System fulfills its public mission as an independent entity within government. It is not "owned" by anyone and is not a private, profit-making institution."

>However, owning Reserve Bank stock is quite different from owning stock in a private company. The Reserve Banks are not operated for profit, and ownership of a certain amount of stock is, by law, a condition of membership in the System. The stock may not be sold, traded, or pledged as security for a loan; dividends are, by law, paid to member banks at a maximum rate of 6 percent, determined in part by each member bank's total assets.

The bank is operated "not for profit", but generates $9x billion in "profit" for the Treasury (as claimed multiple times in this thread).

"Ownership" is a moot red herring. Owning a fictional entity is useless; having claims on its cash flows is not. The Federal Reserve System issues stock to commercial banks and pays an annual dividend to them, before any money goes to the Treasury. It is literally all of the upside with none of the downside (e.g. liability). The investment pays for itself in twelve years and then continues to pay in perpetuity.

The Fed pays its profits to the US government. The chairman of the Federal Reserve board is appointed by the President and approved by Congress. It has statutory legal authorities. It's a little more federal than Federal Express.

The Fed chair is appointed by the government, and profits are returned to the US Treasury. It's independent insofar as the government doesn't have direct control. But they do have oversight, and could legislate it out of existence tomorrow.

Well, Yellen recently said something along the lines of 'being part of the team' and Bernanke claimed something similar in his book or talks iirc ( sorry, no references atm ).

The whole independent claim is just smoke and mirrors.

Maybe a better way to put some Bitcoin proponents' criticism of the Fed would be that they don't like the monetary policy so far actually produced by politics, and would like to use a kind of money whose monetary policy is produced by something else.

I have never come to a particularly clear or detailed position on monetary policy and so I don't know how good or bad a job of it I think the Fed has been doing from my perspective, nor would I assume that Bitcoin or any altcoin is doing a better job. But it makes some sense to me that someone could say "I wish I could use money that wasn't subject to the Fed, because I so often disagree with the Fed".

I've seen some arguments about this that devolved into elaborate discussions about the institutional status and control of the Fed (as this thread might be in danger of doing...), but I've sometimes seen arguments that went in a different direction, where people suggested that it's important for the Fed to be able to set monetary policy for the money primarily used in the U.S., because monetary policy ought to be subject to political control, because it achieves important political objectives.

I tend to suspect that some form of that is ultimately the issue in play at the bottom of some of these discussions: how subject to politics should or must monetary policy be, and how legitimate or illegitimate is it for people to try to use, on a significant scale, money whose supply and interest rate aren't determined by the central bank of the country they live in?

Inflation is only necessary when resources and population are inflating. Because money represents current value in the economy, that amount decreases through consumption or increases from new-found resources. Sometimes deflation is necessary to maintain a balanced money.

Well, even if not keeping everything in Bitcoins (which, I agree, sounds dangerous) the same scheme can be used as a convenient cash alternative that - unlike many credit/debit card payments - preserves privacy. I mean, I rarely want merchants to know my full name or email or whatever, however cash isn't always convenient. The transaction fees aren't great, but it's still looks like a fairly nice option.

(Offtopic) And, sorry, I had just fat-fingered a downvote when I meant to upvote!

True. But, well, I supposed USD-to-BTC and BTC-to-USD services conceal this data to the extent recipient isn't aware of sender's address. This is usually not the case with "classic" services like bank-to-paypal-to-store chain (where PayPal requires you to identify and also would still provide a good insight of your identity to the store).

Also, I think there are coin mixers to avoid this.

OK, but it is actually possible to be extremely private with bitcoin if you want to.

If you use things like bitcoin mixers, or pay/sell bitcoin for cash, it can be extremely difficult for people to track you in a mass collection scenario.

People get away with buying drugs on the internet, or blackmailing people with ransomware all the time and most of them don't get caught.

Sure, if the government is sending black vans to your house to spy on everything you do, you are probably screwed no matter what you do.

But most situations aren't like that. And bitcoin fits the bill for being pretty darn anonymous if you actually go about it right.

> All this having been said would I consider buying and holding some bitcoin as very LIQUID asset, and cash equivalent.

But how liquid Bitcoin really is?

Suppose you have 1 BTC on your phone. Can you instantly turn it into cash (and vice-versa)? Does that depend on a single Bitcoin exchange, which can stop working suddenly leaving you stranded? Does it have to go through your bank account or your credit card account?

This is probably not an issue if you live in a place with a high enough amount of Bitcoin users, since many of them could be willing to exchange Bitcoins and cash with you. But otherwise, it's a relevant question to ask.

Is it more liquid than the stocks I own, yes, and those are the most liquid of my investments (vs bonds, 401k etc).

I live in CA so I have a rather large chunk of cash on hand. It isn't outrageous amount, but I could make it for two weeks if there was an earthquake or natural disaster. I don't think the bitcoin would do me any good if that happened.

Interesting idea, but it feels a bit like "how to use the stock market instead of a bank account". The author mentions fluctuations but seems to think bank fees would be more of an issue - but bank fees could be like $100 at most, where bitcoins could fluctuate all your cash by any percentage at all.

I am also missing anything on the stability of Bitcoin over time. People in Europe, and especially Germany, are obsessed about that, given the experiences of hyperinflation in Germany in the 1920s, when it took 200 billion marks buy a loaf of bread: http://www.usagold.com/germannightmare.html

The Euro may not be perfect, but at least there are rules and institutions working to prevent this happening again.

Actually read the article the author uses CryptoPay which works essentially as a prepaid debit card and provides a normal card that you can use like one from a bank.

I take this kind of articles with the same interest of how to live with $ 100 per month or some other [self or imposed] living with hard constraints: it is insightful but don't try it at home.

Also, when you analyze the details you can discover that using https://cryptopay.me/bitcoin-debit-card takes extra commissions beyond bitcoins (loading fee 1%), so the magic of bitcoins fade a little bit.

...and see your money oscillate around 20% per day with the probability that you can loose it all by having it easily stolen by some hacker or having bitcoin value completely crash.

There is this group of people that had higher education and are well versed in system security, they are called sys admins and even they get hacked some times... but here you are trying to convince us to put all our money into easily movable and untraceable bits in some bitcoin wallet claiming it it the safer option we have.

I get that you're not a fan, but exaggerations don't enhance your argument. Over the last 60 days the XBT/USD pair has an average volatility of 1.23 % [1] which is obviously higher than most major currency pairs, but comparable to a many stock markets. That is, many people invest money in securities with similar or greater volatility profiles.

> easily stolen by some hacker

Whilst Bitcoin is obviously less user friendly than fiat currency, an experienced user like OP can make store their Bitcoin in a way that makes it much more difficult to steal than conventional payment systems.

Firstly, using a hardware wallet (with offline backup) will make your Bitcoin almost invulnerable to 'hackers', plus the use of multi-sig can allow one to dial up physical security to very high levels.

Compare that to conventional payment systems like a credit card - all your credentials are on your card! Anyone who handles your card (waiters, cashiers) gets access to all of your credentials, for the life of the card! (Bitcoin's use of public key cryptography is far more sane in my opinion). And any malware on your computer that could steal Bitcoin could also steal your CC information etc. The only reason that this isnt more of a problem is because by using a bank you are paying insurance for your money and the Bank will generally reimburse you for small amounts - this doesn't make the conventional payment system more secure, just more insured.

You tacitly disregarded the points that don't suit your narrative.

1st. It's not the average volatility that matters it's the maximum volatility that you can normally have. This year it only happen once to have 20% it's true. But you have plenty of days where it oscillates more than 5%.

2nd. Bitcoin is much easier to steal than conventional payment systems like reality tells us, not only because of it's lack of security but also because of accountability. It's hacker free reign, you just steal bitcoin and send it anywhere you want and you have no more trouble. In traditional payment systems this doesn't happen like you try to imply, not because it's insured but because we are talking about real money and that money is connected to a name and an address and sooner or later the police will knock on your door or the door of the person that received the goods purchased with the stolen money or card.

3rd. "Firstly, using a hardware wallet (with offline backup) will make your Bitcoin almost invulnerable to 'hackers'": In a site like this dedicated to people that actually understand a bit about computer security. this sentence is just funny.

> I do not accept the concept of “trust”, I don’t know those guys, why should I trust them? On the other hand, with BTC trust is not even considered to be a factor.

That is a strange argument. The value of Bitcoin comes from the trust people have on Bitcoin. If nobody trusts Bitcoin, it's worthless except as a mathematical curiosity.

And after just a few more paragraphs, we see another instance of trust. The author describes leaving most of the money in a hardware wallet. That is, the author is trusting that the hardware is neither malicious nor buggy. A malicious hardware wallet could use kleptographic attacks to exfiltrate the private keys, or derive them from an attacker-controlled seed. A buggy hardware wallet could, for instance, have a "stuck" RNG (like a well-known OpenSSL fiasco), such that the generated private keys are predictable.

The author is trusting people he doesn't know: the designers of the hardware wallet, the manufacturers of the hardware wallet (including workers at whichever factory manufactures the hardware), and even the postmen. Moreover, the author is not only trusting them to not be malicious, but also to not make mistakes (with crypto, even small mistakes can be deadly).

And there's also at least one other problem the author didn't consider, or at least didn't mention: inheritance. If the author has an accident, what happens to the money? And what if the accident is not fatal, but leads to neurological sequels which render the author unable to access the hardware wallets?

Even more likely: what happens if somebody steals the hardware wallet or it gets lost? E.g. It's in a backpack that is left behind. Does the screen display the private key that you can write down on paper (hopefully correctly) as a backup?

Edit: Apparently on first use the device displays a list of recovery codes which would cover it being lost and the inheritance issue (assuming the manufacturer is still around). I'm a bit concerned the recovery is through a web based tool though:

Even if the manufacturer is out of business, you can still access your coins. The algorithm for creating the private key is public (BIP39, BIP32, BIP44), as is the actual firmware source code.

The recovery is through a web-based tool, but the order of the words is randomized and displayed only on the device, so even if someone installs a keylogger on your PC, he would need to know the correct order (since it's 24 words, that's safe enough).

(Disclaimer: I work for SatoshiLabs, the manufacturer.)

But it's not, and I don't. Bitcoin is 100% transparent and reviewable: the code, the transactions. The same cannot be said for any national or bank electronic monetary system.

As a technical person, I'd trust an open source system more than closed source system any day of the week.

It's not that you need to trust the implementation, it's that you need to trust that the currency will remain useful and usable over time. If nobody believes that they can purchase things using bitcoins tomorrow, nobody will buy them today. There's just as much (if not more) blind trust required in bitcoin, because at least fiat currency is backed by a government. Bitcoin isn't.

> As a technical person, I'd trust an open source system more than closed source system any day of the week.

You just said it: you trust. You trust Bitcoin because you can (and perhaps already have) review the code, the theory, the blockchain. But it's still trust, and you probably value Bitcoin only because of that trust.

TREZOR asks for external entropy during the initialization and this one is mixed with an internal one. Even in the unlikely change that internal RNG generator fails, you should be on the safe side.

> The author is trusting people he doesn't know

The whole design is (hardware and software) is open-source. You don't need to trust, you can verify yourself (or ask a friend who can if you are not able to).

> inheritance

When you initialize device it will give you a list of 24 words, which are a way how to recover funds. You can split these words across your family members (using e.g. a Shamir's Secret Sharing Scheme) and once you are dead your family can recover your coins.

>TREZOR asks for external entropy during the initialization and this one is mixed with an internal one. Even in the unlikely change that internal RNG generator fails, you should be on the safe side.

Assuming it actually uses it.

>The whole design is (hardware and software) is open-source. You don't need to trust, you can verify yourself (or ask a friend who can if you are not able to).

This doesn't matter unless you build it yourself. Open source hardware and software specs are irrelevant if you have no proof the thing you are using followed them precisely.

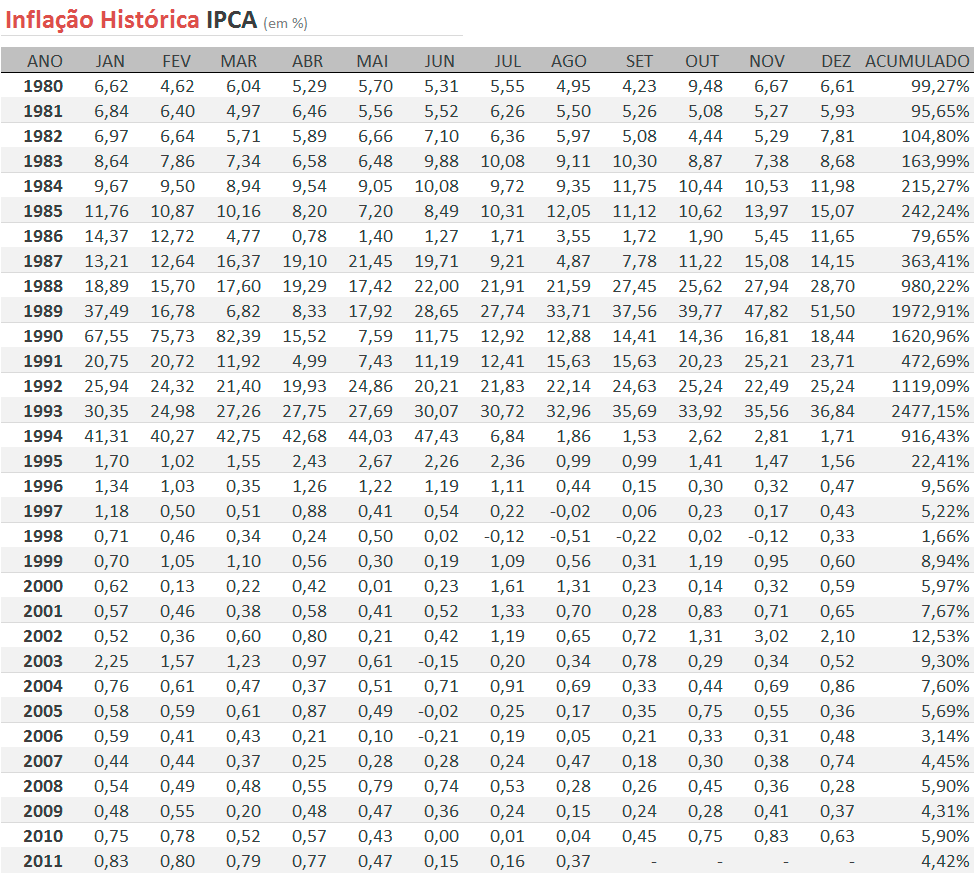

What I don't understand is the extent to which people are paranoid about inflation in Europe or the US. It's low, stable, managed and not a problem unless you're keeping very large amounts of money in accounts which offer inadequate interest. It seems to me that worrying about this or the FDR gold-confiscation collapse of the gold standard is not merely fighting the last war but analagous to hiding in the jungle and refusing to admit that the war on inflation is over.

Residents of e.g. Brazil and Argentina are entitled to a different opinion due to different history, but in those countries people sought hard currency .. the dollar.

When was the last time you tried to rent an apartment in a city (close to the jobs available)?

I'm sure the official inflation rates are low, but when you're looking at real life of real people, they _need_ to move to a big city in a western country to have a normal life and rent a flat there (which is probably the biggest single cost of living).

Seriously, are you trying to tell us that with bitcoin rents wouldn't go up? Are you trying to tell us that rent hikes are not a symptom of gentrification but of evil inflation?

With Bitcoin cash wouldn't be so cheaply available to the selected few. Gentrification means that the demand for urban space is growing. The huge inflation in fiat supply means that more fiat can be spent on buying urban buildings and assets (and stopping urban development). The natural reaction way would be to build Skyscrapers in every city (and blend it somehow nicely with the cities)

Yes .. although housing has traditionally been excluded from consumer inflation measures. There's an argument to be made that housing cost has gone up as a result of cheap credit (although arithmetically that should raise the sticker price while keeping the monthly payments the same), but it also appears to be due to capital inflow. This is the reverse side of the trade deficit with China.

Wow, it's interesting how divergent perspective can be.

Just the other day I came to the conclusion bitcoin is a monitoring tool for the powerful to keep track of advances in digital security by incentivising implicit disclosure.

If someone cracks integer factorization or tsp and thinks bitcoin would be a great way to make some dough on the discovery it will immediately set off red flags to anyone watching.

If your typical nonce is found in a pool of many, but an individual suddenly starts solving blocks and banking 25btc, as of this writing, left and right you'll know straight off that individual has compromised the entire system.

Putting a target on the poor rube's back and destroying any confidence in bitcoin as a currency.

Perhaps this is unlikely but to put all of your trust in a system with such a huge potential to immediate failure terrifies me.

The title of this article ("Hacking Yourself Out of the Banking System and Live Only on BitCoins") reminds me of Colbert's "I am America and so can you". I expected to find title rage in the thread, but apparently grammarians sleep in.

We gave it symmetrical gerunds.

Edit: on second thought, "hacking yourself out of the banking system" is kind of baity and doesn't seem to add information, so we'll take that out.

Which tense do you want to live in ?

— I want to live in the imperative of the future passive participle— in

the “what ought to be.”

I feel like breathing that way. That’s what I like. There exists such a

thing as mounted, bandit-band, equestrian honor. That’s why I like the

fine Latin “gerundive”—that verb on horseback.

Yes, the Latin genius, when it was young and greedy, created that form

of imperative verbal traction as the prototype of our whole culture, and it

was not the only thing that “ought to be” but the thing that “ought to be

praised”—laudaturaest—the thing we like. . . .

..The Prose Of Osip Mandelstam

I also know of a (small but consistent) linguistic practice in which people deliberately speak in gerunds as a form of verbal indirection, and it works surprisingly well.

>linguistic practice in which people deliberately speak in gerunds as a form of verbal indirection

? could you give an example? (I can only think of sentences like "stealing is wrong" - but it doesn't seem like this is what you mean, because where's the indirection?)

In certain forms of bodywork the practitioner will not say things like "breathe deeply" or "pay attention to x", but rather "breathing deeply" and "paying attention to x". I've not studied the origin of this (it may come from trance induction), but it does feel easier to absorb such instructions when they're not issued head-on.

This is wrong. Fiat money is already constantly being significantly devalued. Whether you want to measure it by the rise in exchange value of cryptocurrencies (which, despite constant naysayers that simply don't get it, has been meteoric and constant for the past five years) or the increase in monetary base since the global financial crisis which has inefficiently papered over the structural problems and simply kicked the can down the road for an eventual sovereign debt crisis, or the ongoing global currency devaluation wars that all major fiat currencies are presently engaged in to remain internationally competitive.

There is no valid interpretation of the data which yields the result "Fiat currencies are largely the same value that they were ten years ago".

And having invested in cryptocurrencies from the start and quite heavily, I can assure you that I do not "have big problems" in light of this significant fiat devaluation. Quite the opposite, in fact.

But, I get it, this is HN, and falsehoods about cryptocurrencies and worship of the state and its apparatus are par for the course. I should really be used to it by now but it just continues to boggle the mind that year after year this thing smacking everyone here in the face simply continues to be pushed aside and quietly ignored like it's some weird uncle that is soliciting donations for his satanic church congregation rather than the world changing innovation that it actually is.

So what to you tell people that drank the kool-aid and bought heavily into bitcoin when it was around $1000/btc (to the moon!)? The devaluation they suffered in the period of a couple of months was much worse than what people have experienced with the USD over the last 20 years.

It's this kind of thing that makes me see just how ignorant people actually are about this subject. You have this neat little label you've put on the box and you've never actually done the necessary research to see if your label fits, you heard a headline somewhere, laughed about it and threw it in a mental sock drawer.

Even at a casual glance, your statement is flatly wrong; the peak of the last BTC bubble was 2013-11-30, 1163 USD, a couple months later that bubble had deflated to 826.40 USD, a loss of just over 29%. In the last 20 years, the USD has lost 31.38% of its value, so no, a 29% is not "much worse" than a 31.38% It has rough parity, if we want to get pedantic about it, over the two periods you nominated, the USD actually technically did worse.

But throwing aside that shallow criticism that you happen to be flatly wrong because the statement you made is technically incorrect, and instead focusing on how one would assuage the sense that one had made a bad investment purchasing at that particular point in time, I would say the same thing to them that I would have said to those that had bought at the peak of the bubble prior to that at 220 and then saw a price collapse to half before stabilisation, and then onwards to the only bubble price you're dimly aware of from your shallow knowledge. Or the same thing that I would have said to the people that bought at the peak of the bubble prior to that at 30, which then collapsed down below half before proceeding on to 220 and etc, and that is

"That's how markets work, and if the trend follows and the next time it quadruples the previous high you will be the one talking about how you got in for a steal at 1163 to people who bought in near a peak of 5000 assuming the trend continues, and so on, and so forth".

What I'll say to the person who is all in on fiat currencies over the next twenty years though, is that if everything goes according to plan, they will be subject to the exact same devaluation that the person in their situation was twenty years ago, and that's the optimistic projection. The pessimistic projection is a lot less rosy, and involves a massive sovereign debt bust and the collapse of fiat currencies and the corrupt world central banking apparatus, all expenses paid courtesy of your shallow, misplaced faith in the benighted institutions of the modern status quo.

>Even at a casual glance, your statement is flatly wrong; the peak of the last BTC bubble was 2013-11-30, 1163 USD, a couple months later that bubble had deflated to 826.40 USD, a loss of just over 29%. In the last 20 years, the USD has lost 31.38% of its value, so no, a 29% is not "much worse" than a 31.38% It has rough parity, if we want to get pedantic about it, over the two periods you nominated, the USD actually technically did worse.

Are you listening to yourself? You just compared 20 years to 2 months, and they were approximately equal. That's terrible. Follow it out until the fall of 2014 if you like and it has declined another 50%. Add another few months an in a year from december to december, your wonderful currency has lost nearly 70% of its value. But wait, there's more, let's say you loaded up then because you have so much faith that this is the future (TM). Ride it for just another month and it will lose 30% of the value between December and Jan (~$330->$220).

Methinks you also forgot that money in a bank earns interest and you forgot to deduct that from your devaluation of the USD. $1000 USD in a savings bank in 1996 with a withdrawal now would be about $1500, which essentially nullifies your entire devaluation when talking about holding value over long term.

>would assuage the sense that one had made a bad investment purchasing

Currency is not supposed to behave like an investment. For it to be useful to real humans that depend on it for living day to day, it cannot behave like that.

>price you're dimly aware of from your shallow knowledge

You don't need to pretend that it takes a very complex understanding to recognize an unstable financial instrument. Also, trying to insult people into accepting your views very rarely works.

>The pessimistic projection is a lot less rosy, and involves a massive sovereign debt bust and the collapse of fiat currencies and the corrupt world central banking apparatus, all expenses paid courtesy of your shallow, misplaced faith in the benighted institutions of the modern status quo.

If all currencies collapse, there is little evidence anyone would accept bitcoin instead. Also, a massive debt bust across the global financial system would imply a shortage of cash, not a surplus (a.k.a. deflation and not inflation).

> Are you listening to yourself? You just compared 20 years to 2 months, and they were approximately equal. That's terrible.

You compared them, and your comparison was technically incorrect, so I pointed it out. Price discovery in new class of asset vs the premeditated inflation of a centrally managed fiat currency are different, but it was not I who nominated the two things to compare nor the two periods over which to compare them, nor made a technically incorrect statement about the result of such a comparison.

> Currency is not supposed to behave like an investment. For it to be useful to real humans that depend on it for living day to day, it cannot behave like that

A cursory glance at the historical ubiquity and utility of non fiat currencies would suggest that this is not correct. A simple observation that the inevitable fate of every flat currency that has ever existed has been demise would do so more strongly.

> You don't need to pretend that it takes a very complex understanding to recognize an unstable financial instrument. Also, trying to insult people into accepting your views very rarely works.

Giving me a source for a narrow singular slice of data on the bitcoin price does not negate or address the core point I made about the long term trend being dramatically upward, not allowing for cherry picked time window periods in which things did not align with that trend.

I do not care that you don't accept my views, I care that you make flatly wrong statements based on shallow knowledge and smugly pretend towards understanding and in so doing contribute to the ridiculous smokescreen regarding this particular topic in this particular forum.

Frankly I don't care if people like or dislike bitcoin, I'm simply sick of the lies, falsehoods, and other generally misleading junk that passes for information on it here. Perhaps I should attempt a technically correct assassination of the project simply so people who object on other grounds can at least avoid parroting flat abject falsehoods.

> If all currencies collapse, there is little evidence anyone would accept bitcoin instead

In all the aforementioned cases of the inevitable death of fiat currency, trade and commerce did not simply cease, non fiat currencies took over. There is no reason to assume a change to this pattern.

>A cursory glance at the historical ubiquity and utility of non fiat currencies would suggest that this is not correct.

Such as the tulip bulb? Or spices? There are very few things that have stored value in a long term fashion and that's because they are rare in nature (e.g. gold, silver). Bitcoin's value relies entirely on faith in the system that places arbitrary computational constraints on generating new units of currency. It is still a currency controlled by people.

>I do not care that you don't accept my views, I care that you make flatly wrong statements based on shallow knowledge and smugly pretend towards understanding and in so doing contribute to the ridiculous smokescreen regarding this particular topic in this particular forum.

It was not flatly wrong. You did not account for the fact that currency in a bank would have appreciated due to interest. It seems you lack a very basic understanding of how the current banking system works and have dedicated yourself to pump bitcoin rather than objectively compare it to the existing system.

>In all the aforementioned cases of the inevitable death of fiat currency, trade and commerce did not simply cease, non fiat currencies took over. There is no reason to assume a change to this pattern.

There has never been a case that wiped out all government currencies at once, which is what a 'massive sovereign debt bust' implies. Perhaps you meant something else and failed to convey it.

If you are referring to one currency collapsing, then usually what happens at this point is people just use currencies from other countries. Trading in commodities is a nightmare and would only be the result of massive global instability, in which case the bitcoin network would likely be taken down (or would fork several times) due to countries severing Internet connections.

You have no facts. Merely an ideology you are wedded to and will insist on pushing regardless of the facts even when directly confronted with them, and having simple mathematical statements you make proven wrong. If the facts damn the state, people like you damn the facts, and therefore there is no reason to discuss anything with you.

This is not a rage quit anymore than realising that confronting a Christian with the fact that various points of their faith are simply scientifically impossible and thus factually incorrect. We are playing different games and care about different things. You don't care about truth and I don't care about your political agenda.

We start from completely different premises and have zero regard for the premises of our opposite, therefore discussion is useless.

Your comments are breaking the HN guidelines by being uncivil. We ban accounts that do that, so please don't do that. Instead, edit the uncivil bits out or don't post until you can comment without them. This is especially important when another person is being wrong and/or provocative.

The parent accused me of being a shill and I said that was a childish way to end an argument. The civility guideline is this:

>Be civil. Don't say things you wouldn't say in a face-to-face conversation. Avoid gratuitous negativity.

If someone called me a shill to my face, I would call them childish in person as well.

Can you let me know what I said that resulted in this threat of banning? I will be happy to stop commenting on this site and show myself the door if I cannot respond to accusations.

Your comments in this thread have been egregiously uncivil, and this one is so far over the line as to be a bannable offense. We don't like to ban longstanding users, but if you keep doing this, we'll have to. So please (re-)read the site guidelines and keep your comments civil and substantive from now on.

I spent five years fruitlessly trying to improve the current banking system (actually, the current money transfer system) so I am more intimately aware of its shortcomings than most people. Considering how many things are wrong with it, it's astonishing to me that it works at all. And yet, most of the time, it does.

There are two things that make the current banking system robust: first, because anonymity is limited, most of the actors in the system are honest. Trying to pull a fast one is risky, and that prevents most people from trying. And second, there are humans in the loop that you can appeal to when things go wrong. Most of the time this keeps the system humming along despite the fact that under the hood it's all held together with spit and baling wire.

Bitcoin is the exact opposite. Because it provides greater anonymity than the traditional banking system, it attracts dishonest actors. For example, bitcoin has made ransomware more economically viable than it was before. And second, if something goes wrong with a bitcoin transaction, you are totally hosed. Your bitcoin payment is only as safe as your ability to reliably bind a bitcoin address to an intended recipient. If you get it wrong, there's no recourse. If you accidentally send some bitcoin to the wrong address, you are hosed. If you lose your private key, you are hosed. Period, end of story.

If I have to choose between bitcoin and traditional banking I'll take the latter simply because it's generally more robust and forgiving of everyday human foibles. But I'll continue to wish for (and work towards) a system that gives us the best of both worlds.

Well, we could try to create infrastructure around bitcoin which would solve the problems related to human error, something like delegating sending/receiving to 3rd party which has nice UI and double checks everything. It could also store your private key. You might say that this 3rd party can be hacked -- true, but the same applies to traditional banking.

> we could try to create infrastructure around bitcoin which would solve the problems

Of course you could try, but (I predict) you will fail. The problems I've cited are fundamental problems that are built in to the bitcoin protocol by design. You can't patch your way around them.

For example:

> which has nice UI and double checks everything

How exactly are you going to "check everything"? Remember, you have to get it 100% correct. Failures are completely unacceptable because failures are completely unrecoverable.

Banking run by humans has fundamental problems as well, that's why things like bitcoin come to existence. It is just a matter of tradeoffs.

AFAIK, most of the errors happen because users mistype the address or confuse the commission fee/amount fields, etc. UI could possible introduce some validations for fee/amount issue and probably require to retype the address or something else to avoid the other issue. Another issue is fraud, but it is a unavoidable product of such system, otherwise we end up with same problems traditional banking has. Fraud check means someone might deny the transaction even if your transaction is completely legit, for example, just because you are a citizen of a blacklisted country (my experience).

It is easy to dismiss bitcoin when you are a citizen of 1st world country -- because you are insider and have full privileges, but when you are outsider, it gets very complicated and things like bitcoin give some promise.

> It is easy to dismiss bitcoin when you are a citizen of 1st world country -- because you are insider and have full privileges

That is a very good point, and very easy for someone like me to lose sight of. Nonetheless, I think the answer is not to hand over the final arbitration authority to an algorithm, but rather to design a system where there is an open market in trust. Starting a bank should be as easy as starting a blog. The trick is to come up with a system of checks and balances so that someone who runs a crooked bank can be immediately and unambiguously called out.

The Bangladesh bank heist is perfectly consistent with the GP. You can expect small amounts of large theft (which likely affects users indirectly) or a large amount of small theft targeted directly at users.

> $81M was stolen the Bangladesh Bank via the SWIFT

Nearly all of which was later recovered.

> The IRS Seized $107,000

> DOJ's 'Operation Choke Point'

Those are political problems, not problems with the banking system. If the government decides to fuck with you, then you're fucked no matter what the banking system looks like.

> MasterCard Cuts Off Wikileaks

This is a real problem, and it a result of what is IMHO the main unaddressed flaw in our current system: banking is conflated with money transfer. Bitcoin does address this problem, but IMHO it doesn't do it very well. The risks and costs are too high.

> Those are political problems, not problems with the banking system. If the government decides to fuck with you, then you're fucked no matter what the banking system looks like.

I disagree. Has any government shut down a Bitcoin address for "structuring", or publishing pornography?

Sorry I guess I wasn't specific enough. I was referring to the cryptography that makes bitcoins untouchable to anyone except the person with the private key... not some guy's crappy opsec.

But let's put this in perspective. MtGox lost BTC600k. As a fraction of the primary money supply, that loss was comparable to a USD loss of about $35 billion (M0=$1.2 trillion). So even before most of the Bangladesh money was recovered it was only 1/30th the size of the MtGox loss. And MtGox wasn't even a theft, it was simple mismanagement. Imagine the attacks people would start to mount if they could net the equivalent of $35 billion (or more) risk-free.

I think you're conflating Bitcoin (the system) with Bitcoin opsec skills.

Yes, I agree: Bitcoin is probably easier to steal from people who don't know what they're doing. (And yes there is probably is smaller chance of the thief being caught).

But as of now, properly secured Bitcoin can't be stolen by any criminal, government, or bank. Even if they have physical access to the owner's shit!

The same cannot be said for any modern national/fiat electronic monetary system.

Well if the Bangladesh Bank was also following proper security protocol the money couldn't have been stolen as well.

The 'tech' is, more or less, the easy part. The hard part is all the people involved, and getting them to follow the rules. Sure, you make the tech more resilient to human 'error', but things like MtGox (or Bangladesh Bank) still happened.

The fact that it happened at all (and without McLellan being proven guilty of anything!) is indicative of a severe security flaw in the banking system.

What do you think about a compromise system? Centralized entities that you give trust to, that are run by people, that "know" you - basically a bank - which is using bitcoin as a currency and infrastructure for dealing with that currency?

If you look at it from high above, it would be like replacing the implementation of the current banking system with a more modern stack, but still leaving a similar human interface with the same level of features.

There are some people arguing in this direction, with the construction of settlement blockchains, but obviously the proof-of-waste system would have to be discarded.

I'm all for compromise, but I don't think it's possible to build a compromise system on top of bitcoin.

I think the Right Answer is to have an auditable public ledger maintained by a trusted third party. This could be the government, or it could be a private party, but the key to making it work is to make electronic money storage and transfer a commodity provided by what is essentially a public utility.

"If you get it wrong, there's no recourse. If you accidentally send some bitcoin to the wrong address, you are hosed."

Although this is true, the fact is that in practice this is rarely occurring. No system needs to be absolutely perfect to compete reasonably with the legacy financial banking system. As you point out yourself, the banking system has flaws, and yet it kind of works. Ditto for Bitcoin: it's not perfect, but it works quite well at solving certain real-world problems.

I think theft of Bitcoin private keys is a more serious problem than accidentally sending coins to the wrong address, however this is being solved by hardware wallets, N-of-M transactions, etc.

Mainly because wallet spoofing is not yet lucrative enough for hackers to put a lot of effort into it. If BTC really does start to get major traction, then it is only a matter of time before the web will be flooded with bitcoin wallet spam and phishing attacks.

> Your bitcoin payment is only as safe as your ability to reliably bind a bitcoin address to an intended recipient. If you get it wrong, there's no recourse.

Maybe im being totally naive.. but how about a second blockchain called the "rollback" blockchain.. Suppose you put a "timer" in the bitcoin blockchain for a period lets say 48 hrs..

So when the timer expires, the first blockchain(the coin blockchain), would check for a "rollback transaction" in the second one.. if its not there, the transaction on the first blockchain would be confirmed, and the funds would go to te right account, in a completely automated way, with all the trust garantee that the blockchain tech can give.

Is this a stupid idea? (i just gave a quick tought about this)

OBS: of course, say goodbye to instant payment.. but with double check security sugar on top of it.

Yes, frankly a stupid idea. The current 30 minutesish confirmation time already kneecaps bitcoin. You want to make it 48 hours? Might as well mail a bloody check!

Ok, the time period was just arbitrary.. the most important part of the idea, being a second blockchain to have programmable parameters specifying certain conditions to the first blockchain..

So i dont know what parameters would be the best giving a certain context..

The concept you're describing is called a "smart contract." There isn't a second blockchain, but the transaction itself specifies conditions that must arise before the funds move.

Yes, i think a "smart-contract" would do the trick.. with the plus you could define more arbitrary parameters, to model some context that fits your need.

But the coin blockchain would at least to have a little context about the second one, the "smart contract" one.. binding/linking the transactions in the second blockchain to itself.

Almost all the downsides you listed apply to cash as well which is why people don't keep cash under their mattress anymore and don't do large cash transactions.

Bitcoin should be seen as a currency first and a payment system second. Nothing should prevent the current banking system from adopting it as a currency while keeping all their existing checks in place. Credit cards could support BTC denominated payments and still have all of their chargeback policies in place.

In that world, doing a large Bitcoin transaction would be the analogous of moving trucks of cash around and keeping a large amount of Bitcoin would be like hiding tons of cash in under your mattress (reserved for experts). The majority of payments would be "off chain" while still allowing for people to opt out.

You might ask what's the point of Bitcoin then? Well, I think it would still have a couple of benefits over traditional currencies like USD:

- Supply of currency not controlled by any government or entity

- Easier to "opt out" from system than with physical cash

- Transparency (institutions that wish to do so could use the blockchain to be transparent about their finance)

- Efficiency (though there's been a lot of criticism about the energy consumption of Bitcoin mining, think of all the human capital, real estate and transportation cost that goes into physically moving and securing cash)

>Transparency (institutions that wish to do so could use the blockchain to be transparent about their finance)

This doesn't apply if many of the transactions happen "off chain" to offer the reversibility benefits you mentioned before.

Basically, to get all of the trust benefits of the banking system, you are saying we have to essentially not actually use bitcoin, which makes me wonder what the point is. At that stage, why not have gold denominated credit cards? Less technology to depend on and the government still doesn't control supply.

It's transparency with the bank reserves. With a bank, you actually don't know if there is gold in their vault unless you go and verify if the gold is in the vault. A consortium of banks can also multi-sign an address, so a certain amount of key holders will have to sign off to move the bitcoin, decreasing risk. Then you can use the bank's services to have the equivalent of credit cards, fast off chain transactions and so on.

I guess a similar gold vault problem is possible with private key control, but that is the same as verifying if the bank still has the keys to their gold vault, a much smaller problem.

It's called fractional reserve banking because they don't have gold in their vaults, except for specific ratios. Very, very few banks have gold, instead they have government bonds. They don't have those in 1:1 either.

In the EU: 2.5% of the value of your deposits the banks own in bonds.

In the US: complex, but let's give a simple, not that wrong answer : up to 10%.

In Australia: 0% required, but in practice the banks have a little bit.

That's all the banks have. In our current Bretton-woods economic systems, banks create (and destroy) money.

> This doesn't apply if many of the transactions happen "off chain" to offer the reversibility benefits you mentioned before.

Large institutions as in banks for example who do make "on chain" transactions but I agree this was not the strongest argument. It is correct that transparency goes out the window as soon as your transactions are "off chain".

> Basically, to get all of the trust benefits of the banking system, you are saying we have to essentially not actually use bitcoin, which makes me wonder what the point is.

Yes, in the same way that you are not using "federal reserve notes" when using any of those services (Paypal, credit cards, wire transfers, etc.). Yet you seem to still see the point in USD, the currency.

> At that stage, why not have gold denominated credit cards? Less technology to depend on and the government still doesn't control supply.

It was the case for a long time that fiat currencies were backed by gold. To be honest, I'd be somewhat happy with that but I believe Bitcoin has several properties that make it superior to gold (e.g. it's digital).

Similar to what happened with voice communication, the financial infrastructure will suffer an inversion[1], the banking platforms will run on top of a global value-transfer protocol, instead of the other way around. What you describe at the end of your comment already exists, bitcoin exchanges are using a federated bitcoin sidechain[2] to transfer funds between themselves within their own consensus rules (they could implement reversals or any other feature without having to break the bitcoin consensus).

I don't think difficulties are involved here at all, lowering costs generally translates into higher profit, that should be enough to invest in new technology.

While I appreciate the time it must have taken to write this article, the credibility of an article that recommends services and provides affiliate links in the recommendations is severely degraded in my opinion.

As long as you have to interface with "the fiat world" for income and spending, this sounds like more trouble than it's worth.

The gateways (fiat->btc, btc->fiat) know your identity, take a higher fee than banks and you still have to trust them. Additionaly, you now have the risk of varying exchange rates at multiple points in your money flow.

As for the global bitcoin adoption, I don't see this approach helping at all. If you think of yourself as a node in a global economy graph, you still take fiat as input and produce fiat as output.

>373$ and 479$, which might seems a lot but if you move your BTC at the right time you’re not going to lose anything, on the contrary, compared to the fees you would normally pay for Bank transactions, chances are you’re going to spend way much less anyway.

This is INSANE. Justifying monthly 30% swings in the value of your currency with "bank fees suck" is complete nonsense. Currency instability like that destroys economies because people lose the ability to budget and they become fearful.

In the worst periods of inflation in the US, the currency never devalued by 30% in a month. That's Zimbabwe level crazy.

Also, I pay precisely $0 a month in bank fees, as do many other Americans, so that argument would fall flat even if the swings were much smaller.

{kind=link}

reply