Is this an attempt at juicing Q4 financials? Is this normal among automakers, or is it just a short-term attempt to pump up sales numbers today, at the cost of sales in Q1? Or is this aimed at pulling in market share from competitors?

Q1 sales will be great, some subsidies are coming to boost EVs. But the Q4 are driven to be somber by the subsidy start date; so they’re anticipating some of that windfall to avoid negative press, smooth operations and keep customers from slipping to competitors when demand will bounce January 1.

It's a used but not common practice in the North American car market. Toyotathon happens in December in order to dump old stock and increase sales during the last possible part of the year. Same with the December To Remember sales event from Toyota's luxury arm Lexus. Ford and GM don't usually engage in this unless they're axing the model anyways (Pontiac Solstice and Ford Taurus for example). Happy Honda Days is the only other one I can think of that's recurring. Mercedes-Benz and BMW are irregular with this practice, and BMW only does it with certain models when they do participate.

Probably not, but since TSLA is a highly traded, and somewhat overpriced and volatile stock, it makes sense that every little piece of news will make it move.

Likely not. It seems to be more of a supply practice in order to promote lot turnover and prevent previous model years from sitting on the lot rather than help the company's finances directly. There's a perception that if an older model year car is on the dealership lot brand new, either the model is undesirable or that specific car has a defect. Unfounded or not the brands don't want that association.

It _could_ be good news for Tesla, in that it means they can actually sell to all of their potential customers. Being supply-side constrained is usually a bad thing for a stock’s share price.

Mind you, something’s inarguably up with the share price, even if it isn’t as simple as this discount.

That's some pretty interesting mental gymnastics right there. It could be good news, but most CEOs would interpret their stock price tanking as a result of having too much inventory as bad news. And those other brands can usually sell to their dealers so they can recognize the profits, Tesla can't do that hence these consumer discounts. And it isn't the people that wait for next year that are buying Tesla at this discount either, but it is the people that bought one two weeks ago that feel screwed by this extra discount that they have foregone by supporting Tesla in what arguably must have been one of its most difficult times so far.

_Could_ be good news, yes...if Tesla's share price was not at "assume they can still grow their market share 10X, plus enjoy 10X the industry-average per-vehicle profits indefinitely" heights.

As is - the discounts bear a disquieting resemblance to cold facts contradicting those optimistic assumption.

There is an assumption that Tesla has peaked as competitors are successful in gaining market share. Rivian's successful of Amazon launch [1], Lucid is starting in Europe [2], and NIO is opening up in Europe.

Is Tesla, given that scenario, really a 372B company (as of Dec 23rd) or rather a 45B company like Ford and GM?

I think Tesla gifting the pickup truck market to Rivian and Ford w/ their Lightning is one of the biggest own goals in a long time.

And I think Tesla should worry less about Lucid, etc than Volkswagon working out the kinks in their id.4 (what a terrible name that is), and Toyota's revamped Prius, which looks like a very appealing bridge car that can still use gas on road trips.

Your phone does not contain anti-lock break control, differential torque control, engine tuning control, or the huge amount of other automotive control software that's in a car. You're mistaking the user-facing software (infotainment) for the totality of the software in the car, when in reality it's a minority.

I love how you're listing Rivian, Lucid, NIO, but you're completely discounting the company that has invested tens of billions of euros into an EV platform, and will invest tens of billions of euros more over the next few years.

VW.

FYI, Mercedes, BMW, Hyundai/Kia are also building huge EV platforms. I don't have sales numbers for them, but I imagine all of them are already selling tens of thousands if not hundreds of thousands of EVs, each.

Maybe they're not sold in the US? That would explain some of the comments here.

Someone needed to bootstrap the charging infrastructure. At some point it will be a commodity and at that point Tesla is 'just' sitting on a big asset.

Irrelevant the EU in their benevolent wisdom has mandated that charging networks have to be interoperable.

You can use Tesla superchargers for your 20k Kia economy box.

This is great for consumers with the assumption that Tesla will still find it profitable to build out the infrastructure at all. On the other hand, Europe is a lot smaller, so maybe it doesn't matter as much.

My own country has several charging networks and Tesla isn't even the biggest.

I imagine Tesla owners want to use other networks as well. I wouldn't want to buy a car that only refuels at Texaco.

Europe's charging infrastructure is more developed than North America's. Because Europe adopted CCS Type 2 Combo as the common charging standard many companies can build out chargers:

In the USA, everyone else but Tesla is doing CCS (they might also do whatever the leaf wants also, but usually with CCS). The problem is that Tesla has as much charging infrastructure as everyone else combined (and perhaps even more), especially out west where charging infrastructure is weaker due to less population density.

I guess so, but just because some sweet subsidies are coming January 1 so everyone is procrastinating orders to that date.

In practice it’s just Tesla “chipping in” a bit of the profit boost it will get next year, to avoid ruining their quarterly sales metrics.

Either way the TSLAQ crowd will have a field day with all the negative attention Musk is getting: they’re toast, they can’t sell without discounts, they’re not a carmaker but only a subsidy taker.

> TSLAQ (pronounced "Tesla Q") is a loose, international collective of largely anonymous short-sellers, skeptics, and researchers who openly criticize Tesla

Musk has a habit, a la Boris Johnson, of "snowing" search results that are likely to be unfavorable with his own (Johnson made a big show of repeatedly talking about "painting wine boxes to look like buses" to distract from a campaign issue about Brexit and contentious claims painted on buses).

"Did you mean Tesla Model Q?", might say Google in the future, when someone looks for Tesla Q.

I've never been particularly convinced of the whole "he says he paints buses so that the brexit bus is pushed off Google" thing. It seems like the sort of thing that sounds right, so everyone starts repeating it, but really, is there any evidence at all?

It could be entirely coincidental but he also proposed a bridge between Northern Ireland and Scotland which was a useful distraction from his Garden Bridge which wasted somewhere in the region of £200M.

Sure, also Musk’s behavior on Twitter is bringing a lot of negative press, and the fact he liquidated a ton ton of host TSLA stock to finance the operation.

But indeed markets are not exclusively driven by rational thinking, just look up “head and shoulders” in the context of stock charts. WTF is that? Horoscopes? SMH

Markets aren't rational, but they also aren't stupid. if this is really just a "pre-discount" on the January subsidy, wouldn't that be priced in? It could be less informed retail investors panic selling due to Musk related news, etc. But a panic sale is a panic sale, regardless of the cause.

And, why would they need to do this if the subsidy is likely to kick in on January 1st? They're offering this major discount to increase sales in the two week period between now and the new year? From what I can see it isn't even 100% certain that they'll qualify for the $7,500 subsidy. Maybe there's something about corporate accounting or whatever that I'm not understanding here.

The discounts are happening because of the Inflation Reduction Act that take effect in 2023. The IRA would give a $3500 tax credit for purchasing an EV, like Tesla Model Y.

It takes about ~6 months for people who order a Tesla to get it delivered. For people who ordered in June, they want the IRA tax credit so many considered cancelling or delaying taking delivery until 2023.

This Tesla incentive is to make those people take delivery in 2022 Q4 so that quarterly earnings report would smooth out, instead of dead Q4 and huge spike in Q1 2023.

Edit: my parents are taking delivery this week and are now super happy. They considered cancelling a few weeks back knowing their delivery date was 1 week before 2023.

Why would you want to maintain Q4 sales at the expense of profitability unless it is to maintain stock price though? And as it's obviously having the opposite effect there's no good reason for doing that.

1. Employees, esp the ones with more authority and up the management chain, has a lot at stake in stock compensation.

2. Having and holding inventory, while not bad, creates a whole slew of internal supply chain challenges. Unsure if Tesla as a company actually knows how to deal with that well since most of their existence has been not holding any inventory of completed vehicles. It could cause company problems that would cost way more to deal with than they have people & investment to fix it with.

Agreed, but literally everything else would have been a better option than letting Musk of all people buy it.

It's been a bad run for everyone involved: a lot of the people who built and ran Twitter are without a job, those who had to stay (H1B) are ruthlessly exploited now, Musk has lost a ton of his net worth because of TSLA tanking, TSLA investors lost a ton of money as well, and society didn't benefit from the return of high-profile neo-Nazis as well.

We need to update anti-trust regulations to make sure rich individual billionaires don't have the ability to buy or control major communications platforms, no matter if it's social networks or newspapers. In the end, there's nothing positive about that.

Yeah. My biggest issue with Mastodon is that you can't import your past Twitter posts, or that old posts won't be moved when migrating to a new instance. At least thanks to Fedifinder and other tools, finding your social network again works somewhat...

Twitter was on track to profitability after years of slowly building good will with advertisers and regulators.

Then Musk saddled it with billions of debt, fired all the brand safety and policy people and dismissed advertiser's concerns. So they have paused their ads and redirected spending back to Facebook/Google.

Which is why it is such a perilous state now. Collapse in revenue, extra billion a month in interest repayments and regulators hovering around.

I don’t understand why Tesla needs to rush deliveries at the end of every quarter/year. If they need to provide incentives to meet the expectations they’ve set then the market should realize that and price it in, exactly like this, so what’s the point?

Honestly you’ve hit on one of the dumb things about equity markets. In theory, markets shouldn’t care about lumpy numbers since you can always borrow to smooth out your returns. In practice, dips and spikes see unwarranted reactions every time so firms will smooth out any figure they can, including dividends.

Markets can't realize anything, they have no sentience. The stock market is a graph of rich people's feelings, always has been. It reacts to rumors, sentiments and data, not reason.

A looped barrel that aims straight at the threads. The tank equivalent of a footgun. Aka TurretLoop, now for $420 at your nearest Tesla dealer, pre-orders only while stocks don't last.

The "footgun" barrel would be an excellent image for a editorial cartoon about Elan.

OTOH, making light of the all-too-real issue of friendly fire can go over poorly with older folks, those who've served, and those who've lost family members.

Several Chinese companies build more. And ICE and hybrid car makers like Hyundai and Kia that are now making EVs left and right make a lot of other cars. So it's a little weird to directly compare just a subset of their business. Hyundai and Kia deliver dozens of different models to dozens of different geographic markets. They absolutely have high volume manufacturing, and there is no reason why they will suddenly struggle with producing high volumes of EVs.

There was a time where I would have bought an Ioniq 5 Limited (When the credit was still applicable and my used car was worth more) but couldn't find one anywhere. I was willing to pay a mild markup (which many dealers near me where charging).

I'm sure they'll be beaten at some point, but as it stands, nothing beats the model 3 on range and price. What is your metric for "best electric" here?

It's the quarter and year end, remove "Tesla shares tank" from the headline and it'd be true for all car manufacturers. Add "Tesla" and BOOM, instant viral article.

I don't think he takes his work seriously enough. He is too busy being a dilettante when it seems like he has the talent to focus on one business and od it well. It almost feels like Tesla Motors can't be trusted as a company fundamentally just because Musk will get bored of running it.

Also looking at history and how things are going at Twitter. There might be real worry of him doing some weird pivot and then rolling it back again. Causing loss of money and trust.

He gets crazy whenever there's a crash crunch, but when it was the Model 3 ramp up period it was much harder. Now he should just do nothing and it would be better for all companies involved.

That's not how boycotts work. If enough people do it you can be sure that Musk will notice, it is the cumulative effect of individual actions that are at the root of a successful boycott.

My money my choice, it discounts the branding value for me which is previously there for Tesla. Now from a utility perspective I don’t think this car worth a premium, others are making EVs as well, and EVs actually has a lower market entrance bar than gas powered vehicles

Activist purchasing is something I will never understand. If a car is a better car for the price than anything else then you are only hurting yourself by not purchasing it. It seems like pure hatred of someone to hurt yourself to make them somehow feel worse because you don’t like them.

I just fined the Tesla share price incredible hard to justify, I know they are a growing company with big ambitions but the numbers just don't work.

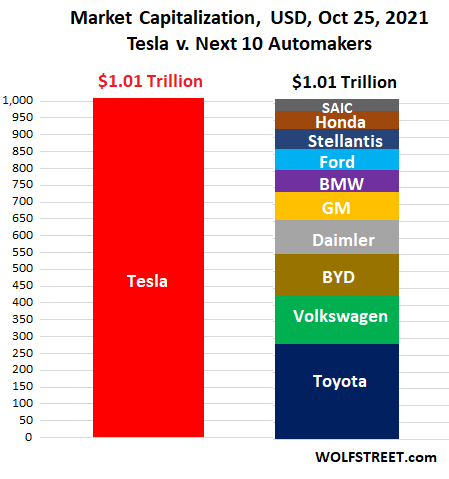

Tesla:

- Market cap: $392.78 billion

- Q3 units sold: 343,000

VW Group:

- Market cap: $70.98 billion

- Q3 units sold: 2,181,300

Obviously they are slightly different companies, Tesla sell solar and battery storage products. And VW Group have brands that sell to a part of the market that Tesla hasn't entered yet.

However there is no way to look at those numbers and make it work. If you go with a market cap to sales ratio, Tesla investors and projecting sales of over 12 million per quarter to match VW...

On VW, they have nearly reached 7% BEV sales, steadily growing. And those cars are well reviewed.

There is something to this. If you include big chunks of Bosch, Siemens and all their other component providers in the VW market cap you would definitely get a more fair comparison to Tesla.

But VWs debt is mostly due to them operating as a bank that sells loans to their customers to buy their cars. So it's more nuanced than just folding the into the calculation. Most other car manufactures don't do that directly.

So Tesla's enterprise value is $426.5 billion and VW's is $473.9 billion?

Regarding the "operating as a bank", are we talking about net debt? I'd guess that if VW loaned money to customers those loans would be assets, right? They wouldn't get the cash from the customer, but they'd get something that looks about as good for their balance sheet hopefully?

The Enterprise Value calculations subtract cash from debt to determine the net debt level. Most think you should also subtract customer receivables as well. In VW's case that is about $150B. So VW's true enterprise value is closer to $300B in my opinion.

Yes, VW does have about $200B in current assets and about $85B in financial services receivables, but that still leaves them with a massive chunk of "real debt" larger than their market cap.

Unfortunately the standard ratios only subtract cash from debt when doing this calculation so this calculation is one you have to do manually if you want to fairly compare car companies.

It's not really about units sold though is it? I guess yes, usually it's a good approximation, but you could sell a single unit for $5bn and have a superior net profit.

Tesla's profit margin looks to be ~15%, whilst VW is at 3% - I'd love to know what it does to those numbers. Tesla's net income for Sept 2022 actually appears to be much higher than VW, if I am interpreting the numbers correctly.

Usually profit margins shrink as volume goes up. You can't sell that many cars into the premium segment simply because the segment doesn't support the volume.

Real sales, yes, but this is why comparing sales by units doesn't mean very much relative to stock price.

Tesla has ~25% margins, VW has 3% margins. A recall, unsold stock or component shortages can quickly put VW in the red. This is what I mean by downturn risk, economic downturn is not the only potential problem manufacturing companies run into.

Tesla has 25% margins because they are in a different segment. If Tesla sold a large number of very cheap cars they would not be able to command 25% margins. If you lop off the top portion of VW's sales and look at their margins they will be much higher than the margins on the smaller stuff. But in absolute numbers those figures certainly help and they also help to protect VWs income stream during slow years.

Their premium brands tend to be hit very hard during those years (Porsche, for instance).

Isn't net profit absolute though, i.e. directly comparable between the two organisations. Long tail of cheap vehicles probably does help VW stay resilient long term (perhaps in the current economic climate / recessions).

It seems targetting volume could be detrimental to net profits under current/recent market conditions. Selling fewer, supposedly more upmarket vehicles has allowed Tesla to out perform VW.

They're simply different companies. VW is fairly broad spectrum when it comes to cars, even a Mercedes 'A' class (or a Smart for that matter) is fairly expensive compared to an entry level VW (say, an 'Up').

Tesla outperforms VW because they are riding a wave and have been very successful in maintaining their lead in BEVs. That won't last and then the likes of VW and possibly Toyota if they ever get with the times are going to eat Tesla's lunch, especially if the chief twat is going to be distracted by his new toys.

The bigger the margins, the more room there is to be undercut from competitors. This is a fundamental property of the free market. When* it works, margins reduce.

*I say 'when' here because too many counter-examples non-functioning markets to list.

Because there is a lot of money to be made selling lots of a cheaper product if you can produce it profitably. Besides that dealers are typically willing to sell such smaller vehicles at or near their own purchase price counting on the recurring income for service and fleet sales of such vehicles tend to be quite profitable because there is only one signature but a very large amount of money involved.

Mercedes is a nice example of a premium brand, they make more money per car and a bit more money in total on lower volume. VW (or rather, the VAG group) is simply a different kind of company. But their profits are nothing to sneeze at.

Because it would make them more money per car but not overall. And they aren't competitive in that segment with the assets they have. They would have to design different models, scale down production etc, a pivot of the company.

A better comparison is Mercedes or BMW, they're in a similar market segment and not selling 10x more cars at 1/5th the price live VW is. Still their market caps are lower than Tesla and their profits are in the same region (depends on which quarter you look at which one is ahead).

That growth is only interesting for two types of companies. One software companies or similar industries where marginal costs are nearly zero, so rapid growth promises huge future profits. And two, companies that could form a monopoly out of that growth to be hugely profitable.

Tesla is neither of those things. So it's not a good long term investment, only a good short term one if the hype continues long enough and you can sell to someone else before profit realities kick in. The tricky thing is that you don't know when that will happen, could be 15 years from now, could be next month.

VW is Audi Porsche Bentley and Lamborghini. I dont know if this ownership is reflected in the stock price of the company listed as VW. Porsche EVs have a better battery performance as measured empirically than Tesla - but they make more modest claims and outperform them, in contrast to Tesla who are essentially lying about battery performance. They are much nicer cars. Porche dealers take care of you very well. Porsche makes very good margin on their cars.

You forgot the supercharger network and the battery factories. Hardware isn't software and those moats are harder to erode, especially for something the size of, well, a car.

1. Tesla has heavily invested in robotics. They will be able to build cars much cheaper than their competitors.

2. Tesla has long-term lithium delivery contracts. They will be able to pay far less for their batteries while the prices for their competitors will massively increase

I have not verified those claims but that would make Tesla's valuation more reasonable.

There is also the self-driving car race. Whoever wins that will take almost all profits. With Twitter, Musk doesn't look too good in the software department right now. However, if you ignore Google, then Tesla still has a chance to win.

> 1. Tesla has heavily invested in robotics. They will be able to build cars much cheaper than their competitors.

Wasn't this proven wrong a bunch of times? Especially back with the Model 3 delivery issues and the "build in a tent" thing? There was an entire period where their delivery woes were blamed on them trying to automate stuff that wasn't worth it or couldn't really be made reliable.

And by the way, if you think Toyota isn't investing in robotics and hasn't been for decades, I have a bridge in Bucharest to sell you ;-)

> 2. Tesla has long-term lithium delivery contracts. They will be able to pay far less for their batteries while the prices for their competitors will massively increase

This would be interesting to read about, do you happen to have a link?

> There is also the self-driving car race. Whoever wins that will take almost all profits. With Twitter, Musk doesn't look too good in the software department right now. However, if you ignore Google, then Tesla still has a chance to win.

Let's discount self-driving cars for the next decade when evaluating any company, I'd say. The tech just isn't there yet.

Bit OT but generally speaking if you care about company culture and want to build something great, acquiring mature companies is not the way to go. You end up with an alien culture you can’t integrate into your own. This is why Apple only buy companies they absolutely have to, and specifically early stage where the culture has not ossified yet.

It can be done with Twitter, the problem was that Elon got too emotional about it. Icahn was already looking forward to a proxy fight and just kicking out people without changing the product too much, but Elon buying his lots of shares was an easier way to make hundreds of millions in profit.

Vw isn’t just cars. They’re are invested in things like Siemens’ energy to be the worlds biggest producer of synthetic fuel. Vw is the big boy and toyota is the big boy in asia. Tesla is valued the same as all the other car manufacturers put together.

Their market share price is speculation from fan boys that want a poorly manufactured usb mouse to drive in that you have no way of fixing yourself or even taking to a specialist.

If you want to make some money in the next year or so, open a short position on Tesla. Not financial advise, just 2 cents from a guy that worked in the motor industry for 15 years

Tesla is priced as a volatile growing tech company, for better or worse. They aren’t priced according to current performance, but predicted future performance.

VW is a known thing, they aren’t expected to get much bigger than they are today, they might even shrink a bit.

Tesla is more of a risky bet, which is why it’s stock price is so volatile.

> If you want to make some money in the next year or so, open a short position on Tesla. Not financial advise, just 2 cents from a guy that worked in the motor industry for 15 years

Short pressure is enormous. It's not cheap to open this position.

The notion of “share price” is something I haven’t ever really understood.

As I understand it, if four people are queueing up to buy stock A for [$10, $9, $8, $7] and four other people are in line to sell for [$10, $11, $12, $13] then the people at the front match up and swap one unit of stock for $10, and the stock exchange lists A as being last valued at $10.

Stock B’s order books have four buyers at [$10, $1, $1, $1] and four sellers as [$10, $99, $99, $99]. Again the matching buyer and seller exchange $10 for one unit of stock, the exchange shows B on its ticker for $10, and we say that company A and company B have the same value.

B’s future looks a lot more bleak. Buyers say it’s a junk stock, only worth a dollar. Sellers claim the company is way under-valued: you need the best part of a hundred dollars to convince them to give up their share.

People say these things in real life — retail investor blogs, Mad Money, fund forecasts etc. — but those are just words compared to actual buy/sell orders. Do exchanges give us insight into what their order books actually look like, instead of just quoting the last price where a buyer and seller matched?

I want this problem to be symmetric in such a way that A and B truly do have the same value, as shown by the market, but something about the $1 buy price for B feels more important than the $99 sell price. I think it’s because buyers have actual dollars — the things we need to buy food and shelter — so what they say is more important than what B’s snake-oil stock-sales people claim.

In the short term, the exchanges tell us how popular a share is, based on hype, trades, etc.

In the long term, over several years, the stock price vaguely follows the value of a company (depending on the exchange - back in Australia you could discover "sure things" a year before the rest of the market was paying attention)

1. For anything remotely liquid, the order book won’t look like this for various reasons.

2. Except at very high frequency time scales there are more robust measures of price that are typically used: e.g. VWAP over some interval (this would be ~$10 in your example), or the clearing price of the closing auction, etc

The scenario you gave is very unlikely for stocks with large trading volume like TSLA. The spread is nowhere near that wide, and if it was market makers would make a profit out of that.

Resting liquidity far away from the best bid offer is close to meaningless. The last traded price contains almost all the relevant information from the microstructure. You can get an additional 0.03 percent notional of pricing information by looking at the what you're talking about.

> Do exchanges give us insight into what their order books actually look like, instead of just quoting the last price where a buyer and seller matched?

They do. I haven't seen depth info past the best bid/offer (maybe exists? I'm not an expert), but I see the bid and ask prices with sizes in my broker's app in realtime. "Last price" is just one useful bit of information.

The theory behind showing the last price is that an actual matched transaction feels less likely to be "wrong" (over short periods) than bid/ask in illiquid cases. Sometimes there really just aren't people on one side ready to buy/sell, and the ”$1 $1 $1” would say something less realistic, not more.

Good question though, dunno why anyone would downvote.

> haven't seen depth info past the best bid/offer (maybe exists? I'm not an expert)

Most exchanges will provide arbitrary depth in way of a pure order feed. From that you can construct your price book, which gives you the levels of depth.

Some just expose the price book, some price book and order feed, some just order feed.

Some anonymize the order feed, some don't (I think typically in equities it's anonymized although not my asset class, but other markets e.g. power need to be de-anonymized and you can see the other buyers and sellers submissions).

However, that data doesn't represent the market price - I would look to constructing the fair price using the trades made on the exchange rather than the outstanding orders. From that you can create different lenses to view the fair price - e.g. volume weighted, time weighted, other types of averages.

There’s been 12 updates to Teslas in the last month OTA, BMW did one in 2022 and any car with iDrive 7 (their first to support OTA updates) had to be taken in to the dealer to do the update.

Also looking at the apps, sending a command through Tesla’s app is instant, meanwhile BMW’s app makes you look at a spinner for 2 minutes.

I’m sure Tesla’s likely cutting corners somewhere to get that kind of performance, but as an end user it’s a great experience.

> There’s been 12 updates to Teslas in the last month OTA

That's not something I would ever want for my car. I don't want my vehicle to be at the end of someone's CI/CD pipeline. I would much prefer say a quarterly cadence of rigorously tested, solid new releases. But, that's more expensive and harder to do, so hardly anyone's doing that anymore for non-critical software.

You’re thinking only about infotainment updates, where for example recently Tesla pushed out an update that increased charging rates, allowing you to charge up quicker.

I couldn't care less about a minor charging rate increase that is so minimal that they don't even give any details about how much its increased.

I'd rather a manufacturer that actually tests and releases fully engineered products rather than winging it with constant OTA upgrades.

Tesla track record of OTA for faulty ABS calibration leading to terrible braking distances and a kludge to try and avoid a recall for faults in their HVAC implementation doesn't sell it as a benefit.

They usually outsourced software to the supply empire, and well, imagine software development, but in a waterfall, bureaucratic, cheapest first wins empire that is trimmed to produce one iterration per car version at best or the ocassionaly at service update.

If you want to become more agile and want to sell software as modules and updates, this quite physical seperate dependcy hell comes back to bite you. Its basically waterfall for every update.

BMW munich software department was famous for having no developers. Just specs and architects. People who were doing software developer "internships" there, were failed at some universitys cause that would have been a "NoCode" internship.

Software in this world was not a living product, thats regularly updated, its a off the shelf part made to specifications.

They tried to change in recent years, in reaction to tesla, but i highly doubt they can pull it off. Maybe in eastern europe, they have a developer/software culture.

Its almost like a very large shareholder knew, and despite saying they were not selling, was dumping shares the last couple of weeks on the hard core believers as quick as they could

If I was an US taxpayer, I would be so pissed off to know that I'm paying for assholes buying a somehow luxury car and Elon getting billions in margin so that he could afford to crash twitter...

As the U.S. government plans to introduce tax credits to spur EV demand starting in January

The US is becoming increasingly protectionist and Tesla is their crown jewel. They'll give Musk a blank check at this point because they're terrified of Chinese auto industry.

{kind=link}

Forget "discounts". Show me the final price as delivered with all fees and taxes included.

[1] https://www.cars.com/articles/tesla-offers-7500-discount-on-...

reply